Since 2013, thousands of clients of Planet Pensions – previously known as Aktiva Wealth Management and Square Mile International Financial Services – have been scammed out of their pensions.

The clients were conned into these transfers on the basis that it would be in the interests of making their pensions perform better. It was also claimed that the clients would pay less tax. None of the promises, assurances and advice was true:

LIES TOLD TO VICTIMS BY PLANET PENSIONS

THE TRUTH

“A QROPS falls outside the Lifetime Allowance rules for UK pension schemes. If your pension grows to above 1.25m you will suffer a 55 percent extra tax charge”

Most of Planet Pensions’ victims had pensions which were below £50k in value and were never likely to reach anywhere near £1.25m in value – so this would never apply.

“At age 55 you will be able to access a cash lump sum”

Had the victims left their pensions in the UK, they’d have accessed the 25% tax-free lump at age 55

“The QROPS is of course approved by HMRC”

HMRC never “approves” any QROPS schemes. They register them – there is no approval.

“Your pension will be invested in funds which are not traditionally available in the UK, giving you access to a broad range of asset classes”

There is a good reason why risky, unregulated assets are not available in the UK – it is illegal to promote them to retail investors. Victims would be likely to lose their pensions (which is exactly what happened)

“With a wide range of high growth asset classes utilised, the high performance funds chosen by our investment team are ideally suited to your pension investment”

None of the high-risk/high-commission assets were suitable for pension investments – and they all failed (destroying thousands of victims’ pensions)

“The investment enables you to invest in investment funds which will contain a carefully managed risk assessed portfolio”

There was nothing to “manage” – once the pension money was invested in the assets, the money was trapped and would inevitably be lost

“A QROPS allows a wider choice of investments, which gives you the potential to grow the fund further than your current scheme”

This is true! Many QROPS allow fraudulent investments such as those chosen specifically for the high commissions paid to the scammers

Of course, none of this – either the transfer (by a UK resident) to a Hong Kong QROPS – or the subsequent high-risk investments, was in the interests of the victims. This was only in the interests of the scammers who earned commissions from the unregulated investments. These included:

In the GFS QROPS scheme in Hong Kong, Planet Pensions worked with a variety of unregulated “introducers” to help recruit victims. These included Scott Campbell of 3V Financial, Andrew Blackburn of St James International, and Aled Williams of Nicholas Street Tax.

The QROPS application forms, which showed which adviser each victim had appointed, were forged to show the name of the introducer rather than the name of the adviser. This was done by removing the adviser declaration page, and inserting a new page showing the introducer as the adviser – rather than Aktiva Wealth Management (one of Planet Pensions’ former names).

Planet Pensions also often claimed that Aktiva Wealth Management was acting under the regulation of Paul Brown’s Worldwide Broker – using the Dutch AFM as the regulator. Paul Brown has strenuously denied that he ever allowed Aktiva (Planet Pensions) to act as an Appointed Representative of Worldwide Broker.

“Missing expat pensions: Some 10,000 people put their money into a financial firm run by advisers who investigators say have transferred millions to their own accounts. Bosses at Brite – led by Mark Donnelly – transferred millions of pounds to their personal accounts or other companies.”

“The savers are victims of a network of financial advisers working for a firm called Brite Advisory Group, which is run by Mark Donnelly, a convicted fraudster who stole football merchandise relating to David Beckham. Donnelly’s right-hand man was a financial adviser who fled UK after duping a 91-year-old dementia sufferer out of £170,00. Investigators claim that instead of investing savers’ money in pensions, bosses at Brite took millions of pounds and transferred it to their personal accounts or other companies they ran around the world. Some of it is alleged to have been used to buy rival businesses; some was used for personal loans to directors and their wives. About £250,000 was allegedly used to buy two Porsches.”

And one of the rival businesses Donnelly bought was Planet Pensions (aka Aktiva Wealth Management and Square Mile International Financial Services. Donnelly paid £650,000 – using Brite Advisors’ clients’ money.

The following blog was written by Stephen Sefton: a Blackmore Global Victim who cares about pension scams.

Stephen was scammed by David Vilka of Square Mile International Financial Services around six or seven years ago. Vilka, who had neither qualifications nor a license to provide pension or investment advice, arranged the transfer of Mr. Sefton’s substantial final salary pension.

Stephen’s pension was transferred to the Optimus QROPS in Malta.It was placed in an Investors Trust offshore bond in the Cayman Islands. Then it was invested in high-risk, high-commission, unregulated funds. One of these was Blackmore Global.

A determined fight on the part of the tenacious Mr. Sefton did eventually result in the recovery of a large part of his funds. But his case was a rare exception. He was, indeed, very fortunate that he didn’t lose the whole lot. Most victims suffer total loss in such circumstances.

It is now looking very likely that Phillip Nunn and Patrick McCreesh’s Blackmore Global Fund is going to be as worthless as their other investment scam: Blackmore Bond (now in administration).

Pension Scam victim Stephen Sefton writes:

Finally, after two months of radio silence, Angie Brooks once again pens an article. It’s about time!

I care. I don’t know why I should but I do. Maybe because I am seeing a media frenzy over the recent collapse of mini bonds in the UK. Especially LC&F and Blackmore Bonds plc to name just two. Meanwhile, victims of pension scams from the last decade are being forgotten and swept under the carpet. Much to the delight of many of those that oiled the wheels of the scams and helped them to happen – especially the QROPS and SIPPS!

There are many (especially the scammers) that really don’t like me. This is why they tried to offer me a paltry £6000 to silence me. Seriously?

There are many that don’t like my rhetoric and I regularly get blocked on Twitter, or thrown off Facebook. Here, I get to tell it like it is, however unpalatable the truth may be.

What I have learned over the years is that there’s an intricate web, woven around these scams. This interconnects a number of players whose names just keep on cropping up.

Malta was clearly the jurisdiction of choice for many pension scams. It seems to have hundreds, if not thousands, of victims. Many of these are not yet even aware that they face financial ruin in their retirement.

In my opinion, Malta has much to answer for and really should clean up its act. Journalists rarely focus their gaze on the real facilitators of pension scams: the Mickey Mouse jurisdictions that turn a blind eye and allow them on their patch.

Why are they not aware? QROPS Scheme Administrators are sending out fictitious statements implying members’ pensions are still intact. One member of STM Pensions Malta was sent a statement in Sep 2020 showing his pension still intact just one month after STM wrote to members invested in Blackmore Global – Nunn & McCreesh’s offshore unregulated collective – that in fact they (STM) have no idea what the value is!

As it happens, STM did manage to get Nunn & McCreesh to publish the underlying assets for Blackmore Global, in May 2020 (over 6 years since the fund was launched). Even with this list, there is little idea what the fund is worth because the underlying assets are themselves useless, opaque, private ventures in yet more Mickey Mouse jurisdictions. One offshore fund is already being pursued by Dalriada as part of other failed pension schemes from early in the last decade – but Dalriada are getting nowhere with it.

I am not convinced that “The Adams v Carey case is likely to herald a flood of similar claims …”.

Courageous Manita Khuller in front of the Guernsey courthouse

The Ombudsman case that went in favour of Mr. N against the Northumbria Police Authority (PO-12763) in July 2018, was also a landmark case against a negligent UK pension provider that had a tick box culture. The ceding provider transferred Mr. N’s pension without due regard for the Pensions Regulator’s requirements of 2013 for extra due diligence when handling transfers.

That decision doesn’t appear to have “herald[ed] a [likewise] flood of similar claims” three years on.

Firstly, the victims were targeted by scammers because they were “ignorant”. That’s not meant to be derogatory.

They knew diddly squat about pensions, regulations, investments – nothing! They trusted the “adviser” – the con man persuading them to transfer their pension. For a con to be successful you need the essential skill of gaining people’s trust. Scammers have this skill in abundance. The ignorant fall for it every time.

Victims not only knew nothing about pensions and investments, they didn’t even know how to spot they were being conned. They were the perfect mark for scammers. They didn’t know what they didn’t know. Like taking candy from a baby – although a baby knows it is being robbed and often screams quite loudly (so maybe not the best analogy).

Secondly, even if victims have now discovered they have lost their pension, they have absolutely no idea what next to do about it. The ones I have come across are like fish out of water. Completely at a loss of where to go.

On Angie’s facebook group, one person recently told of their father’s loss of pension to Nunn & McCreesh’s Blackmore Global. In an attempt to do “something” the person went to the FCA on behalf of their father only to be told that investing in unregulated funds on the advice of unregulated advisers bars them from the compensation scheme and Ombudsman service. The FCA suggested looking into the Malta compensation scheme – which is a joke! That was the extent of help from the FCA. As useful as a chocolate teapot.

It hadn’t occurred to this person that either the ceding provider is guilty of maladministration for the transfer in the first place, AND/OR the receiving scheme in Malta is in “breach of trust” because it too is bound by legislation controlling its activities.

So the best next step is to pursue one or other side of the transfer – or both.

Manita Khuller went after the receiving trustee through the courts and eventually won. However, such legal action isn’t for the faint hearted. It cost her huge sums of money, which she took out loans to fund. Losing was not an option. On top of already losing her pension. It was a nightmare for her. I know – I was with her every step of the way since 2018 when we were introduced by a journalist. This was her only option because the Mickey Mouse jurisdiction, Guernsey, had no “Ombudsman” service. Moreover, the incestuous nature in Guernsey meant law firms declined to represent her. She had to go it alone for the first trial, adding a layer of stress no person should be subjected to. There are few victims with this determination or courage willing to take this course of action – so they don’t, even though she has paved the way.

We in the UK, at least, have the Ombudsman and now – relatively recently – Malta also has one (the Office of the Arbiter for Financial Services (“OAFS”)).

Guernsey is a backward, biased, Mickey Mouse, incestuous jurisdiction – which is why scammers love it.

The Scheme administrators on both sides of the transfer will fight tooth and nail and argue the victim is wholly to blame for their losses. Many victims just have no idea how to go about presenting their case.

There is no “free” professional service available to help victims navigate this minefield. Mr. N (referenced earlier) paid lawyers £25k to make his case. But the Ombudsman did not award costs – saying that it is not necessary to engage lawyers. However, it is not easy to fight a pension scheme that will employ a top notch law firm to present its defence. So by and large, the victims I have come across are at a serious disadvantage because they have no idea how to seek justice and have nowhere to go and don’t know how to present their case. That’s why they were targeted by scammers in the first place. They were (and still are) easy pickings.

In the article above, Ms. Brooks quoted from the appeal. I will do same. A more appropriate section, §115(i),

“… while consumers can to an extent be expected to bear responsibility for their own decisions, there is a need for regulation, among other things to safeguard consumers from their own folly.”

Members of Staff (in shorts!) from Carey Olsen

These victims are indeed victims of their own folly, but they never realised what they were doing. On both sides of the equation (ceding providers and the receiving schemes) there were duties of care designed to protect these victims “from their own folly”. In all cases I have come across, neither side fulfilled those duties of care. On the UK side there was contempt for the Pensions Regulator’s requirements of 2013, despite growing industry concerns for pension scams. On the receiving side, the QROPS didn’t (and still don’t) care about their members – period. And neither did the authorities in these Mickey Mouse jurisdictions. It was the perfect match and thousands of vulnerable victims are paying the price.

Carey Pensions was started in 2009 by the Carey Group. The Group is controlled in Guernsey by ten partners and ex-partners of the Law Firm Carey Olsen. This is an amusing coincidence in my opinion. Carey Olsen, perhaps the top law firm in Guernsey, represented FNBIT against Manita Khuller – and LOST at appeal by the way.

Justin Caffery floating in the sea while preaching stress relief

Harbour Pensions was started by Justin Caffrey, in 2013 and says in the STM announcement, “Harbour was always a five year plan…”. Justin made his money and now runs meditation classes (seriously?). He should meditate on the misery, caused by Nunn & McCreesh, of hundreds – if not thousands – of vulnerable victims of Blackmore Global that he allowed into his pension scheme, in my opinion, willingly and knowing the consequences of such an unsuitable investment. He permitted 100% allocation of one member’s pension into a fund that has never published audited accounts. At the material time, knowing the fund was opaque and unregulated, Harbour (and other QROPS) were happily permitting transfers and 100% allocations.

The fund’s offer document, which Harbour had, says the investment has a ten year lock-in. That condition, which the QROPS knew and willingly accepted, effectively locked Harbour (and subsequently STM) into an asset they knew nothing about – and still don’t – for ten years, with absolutely no knowledge or control of what Nunn & McCreesh were doing with the money.

The Scheme administrators in these QROPS in Malta were, and still are, completely at the whim of Nunn & McCreesh – who could misappropriate the pensions as they wish and the administrators could do absolutely nothing about it. The QROPS effectively abdicated all powers they had to run the scheme and mitigate risks in the interest of members, to Nunn & McCreesh. They have been passive bystanders to the destruction of their members’ pensions ever since. This is, in my opinion, in breach of the Malta Trust and Trustees Act. They are also willingly and knowingly in breach of trust.

All this really begs the question whether STM go looking for dodgy pension schemes or are they just plain stupid? What on earth is going on and why hasn’t the MFSA taken them to task? They seem to attract scams like flies to a pile of dung.

Blackmore Global Victim who cares about pension scams – says victims are being forgotten

Victims are being forgotten by the media and authorities. Victims had no idea what they were doing or how to seek restitution. They are guilty of nothing but ignorance and ALL the actors in these scams have gotten away with it. They have ALL dipped their hand in the pension pots and kept the spoils – and now moved on, leaving the pension pots empty.

This is frustrating in the extreme because I see no evidence of any “flood of similar claims”. The victims are, for the most part, still ignorant and there is no one “helping” them. This site (Pension Life) once purported to “help” victims but I am not at all convinced it has done much and now has long periods of radio silence. The newbies in this scam space, the journalists claiming to be the heroes that “blew the whistle” or warned the FCA, are just chasing big headlines for their editor on today’s flavour of the month: mini bonds. Soon the mini bond victims will be forgotten just like the victims of Defined Benefit Pension transfers. The blood sucking journalists will move on to the next headline. I have no time for these insincere upstarts because they don’t stay in it for the long haul.

Victims are on their own by and large and still ignorant. No one seems to care and there is no help from any quarter. They face a retirement with a significantly reduced standard of living and that’s the hard truth of the matter. There will be no “flood of similar cases”.

Fighting pension scams needs to be done logically and methodically. Decent advisers need to use high standards to help fight scams. If these standards become the norm, the scammers won’t survive and flourish so easily.

Fighting pension scams – Qualifications

Most qualified advisers want nothing to do with pension scams. Many offshore firms employ advisers who have not passed the required exams. Even if an adviser has qualified, he or she must still be registered. We recently surveyed a number of offshore advisory firms:

The Chartered Institute for Securities & Investment (CISI) is the largest and most widely respected professional body for those who work in the securities. The Chartered Insurance Institute (CII) is a professional body dedicated to building trust in the insurance and financial planning profession.

All financial advisory firms should list their advisers, provide clear details of each adviser’s qualifications and a link to the institute’s register showing evidence of the qualifications.

“Qualifications are not the be all/end all. A certificate does not prove professional competence in the field , ethics or experience. But the public have to start their due diligence somewhere.”

and many others such as Westminster and London Quantum – ruining thousands of lives. Several of his schemes are under investigation by the Serious Fraud Office. He also provided the transfer advice in the Continental Wealth scam.

Any decent adviser will want to be fully qualified. And registered. The rest should go back to selling snake oil. But consumers must remember there are exceptions. Some regulated firms get it wrong. Qualified advisers can get it wrong.

Clients must have comprehensive fact finds and risk profiles

Firm must operate adequate compliance procedures

Advisers must not abuse insurance bonds

Clients must understand the investment policy

All fees, charges and commissions must be disclosed

Investors must know how their investments are performing

Firm must keep a log of all customer complaints

Fighting pension scams – why qualifications are so essential

If clients used only firms that tick all ten Standards boxes, it would be harder for the scammers to get business. Decent firms who care about their reputation should make sure there are clear links to all advisers’ qualifications. Make it easy for the consumer to understand how to check that the stated qualifications are genuine. And help educate people to understand what qualifications are required.

All too often, advisers claim to have qualifications that don’t exist – or that aren’t appropriate for investment advice. For example, some advisers who are assuring clients they can advise on pensions and investments, only have qualifications suitable for mortgages. Or worse still, no qualifications at all. Whatever the adviser says his qualifications are, the client must be able to double check.

You wouldn’t go to an unqualified solicitor would you? So don’t use an unqualified financial adviser. Being qualified goes hand in hand with being regulated.

If it was easy to stop pension scams, everyone would be doing it. Clearing up the mess left behind a pension scam is a huge challenge. This is why clear international standards need to be recognised and adopted. The scammers are like flocks of vultures. If people only used regulated firms, they could avoid a lot of scams.

Firm must be fully regulated – with licenses for insurance and investment advice

Advisers must be qualified to the right standard

Firm must have Professional Indemnity Insurance

Clients must have comprehensive fact finds and risk profiles

Firm must operate adequate compliance procedures

Advisers must not abuse insurance bonds

Clients must understand the investment policy

All fees, charges and commissions must be disclosed

Investors must know how their investments are performing

Firm must keep a log of all customer complaints

Why is regulation so important?:

If a firm sells insurance, it must have an insurance license.

If a firm gives investment advice, it must have an investment license.

Many advisers will claim that if they only have an insurance license, they can advise on investments if an insurance bond is used. This practice must be outlawed, because this is how so many scams happen.

Most countries have an insurance and an investment regulator. They provide licenses to firms. Some regulators are better than others. Most regulators do some research and only give licenses to decent firms.

History tells us that most pension scams start with unlicensed firms. Here are some examples:

Continental Wealth Management invested 1,000 clients’ funds in high-risk structured notes. Investors started with £100 million. Most have lost at least half. Some have lost everything. Continental Wealth Management had no license from any regulator in any country.

Serial scammers such as Peter Moat, Stephen Ward, Phillip Nunn, and XXXX XXXX all ran unlicensed firms. Peter Moat operated the Fast Pensions scam which cost victims over £21 million. Stephen Ward operated the Ark, Evergreen, Capita Oak, Westminster and London Quantum pension scams which cost victims over £50 million. XXXX XXXX operated the Trafalgar pension scam which cost victims over £21 million.

Phillip Nunn operates the Blackmore Global Fund which has cost victims over £40 million. Serial scammer David Vilka has been promoting this fund. Over 1,000 people may have lost their pensions.

Firms that give unlicensed advice are breaking the law. Unlicensed advisers often use insurance bonds. These bonds pay high commissions. The funds these advisers use also pay high commissions. The advisers get rich. The clients get fleeced. The funds get destroyed. Insurance bonds such as OMI, FPI, SEB and Generali are full of worthless unregulated funds, bonds and structured notes.

Unlicensed firms hide charges from their clients. Most victims say they would never have invested had they known how expensive it was going to be.

Hidden charges can destroy a fund – even without investment losses. Licensed advisers normally disclose all fees and commissions up front. This way, the client knows exactly how much the advice is going to cost.

People can avoid being victims of pension scammers. Using properly regulated firms is one way. An advisory firm should have both an insurance license and an investment license. Don’t fall for the line: “we don’t need an investment license if we use an insurance bond”. Bond providers such as OMI, FPI, SEB and Generali still offer high-risk investments. The insurance bond provides zero protection. And the bond charges will make investment losses much worse.

Blackmore Bond – yet another reason why only regulated advisers should be used for investment advice.

The clear link between the recently-failed LCF Bond and Blackmore Bond through Surge Group remind us how important regulated investment advisers are.

In the news again is the troubled Blackmore Group. This time we read that they have ‘temporarily’ closed their bond – the Blackmore Bond – to new business. Just a few weeks ago, Blackmore Bond changed the wording of the sales material on this product.

The Blackmore Bond transparency was not due to Blackmore Group having a yearning desire to be honest with their victims. It was all down to new FCA rules for being “clear, fair and not misleading” whenever an investment is promoted.

Recently, there has been a lot of media coverage on high-cost, high-risk bond investments failing. One of these is London Capital & Finance (LCF). This unregulated bond collapsed and went into administration earlier in 2019. £236 million had been invested into it. But investors had not been warned of the costs and risks involved. Of this £236 million, over £50 million was paid to Surge Group for promotional and marketing services.

1,200 victims duped into investing in the LCF bond

have lost at least 80% of their money

Fortunately for investors in the Blackmore Bond, it is still active. However, with such high promotional and marketing costs, the bond needs to be very successful indeed to overcome the initial 20% charges – most of which were paid to Surge.

In relation to the closure of their bond, Blackmore Group state on their website:

“We have achieved our fundraising goals for this tax year and are not currently taking in new investment. We will be introducing our next offering in the following tax year, so please watch this space for future announcements.“

Another questionable investment from the Blackmore Group is the Blackmore Global Fund.

The Blackmore Global Fund has been heavily criticised and also featured on BBC 4 You and Yours. The fund saw 1,000 victims conned into this expensive, illiquid and high-risk UCIS. It is illegal to promote UCIS funds to retail investors in the UK. They are certainly not suitable investments for a pension fund.

David Vilka of Square Mile International Financial Services was one of the promoters of the Blackmore Global Fund. Vilka invested many of his UK-resident clients into this unsuitable fund. Undoubtedly, he was paid fat commissions for these investments. Unregulated and unqualified, Vilka was no doubt lining his own pockets, instead of doing what was best for his clients.

Vilka lied to his clients, claiming to be fully regulated. He transferred his UK-based victims’ pensions into the Optimus Retirement Benefit Scheme No.1 QROPS. Much of this money was invested into the Blackmore Global fund.

The connection between Blackmore Group’s Bond and London Capital & Finance (LCF) is Surge – a marketing agent. The LCF bond was promoted by Surge until it collapsed in December 2018.

After LCF collapsed, Surge went on to promote the Blackmore Bond. This promotion was done using ISA-rating websites.

London Capital & Finance is not the only failed investment in recent years. Other failures include Axiom with £120m worth of investors’ funds (£30m of which was with life offices FPI and OMI); LM £456m (£90m with FPI and OMI); and Premier New Earth (NERR) £207m (£62m with FPI and OMI).

The new transparency demanded by the FCA is much needed.

Unfortunately, it won’t change the fact that well over one billion pounds have been lost between LCF, Axiom, LM and NERR. We are still left wondering why the regulators have not taken a tougher stance on restricting the promotion of such UCIS funds. The FCA’s limp stance is especially worrying when the promoters of these high-risk bonds and funds are targeting UK retail investors.

All these failures and losses should remind both regulators and consumers that only regulated firms should be used for investment advice.

The ceding providers have something significant in common with the scammers. When we expose some of the scammers, their lawyers swing into action. I once had letters from Carter Ruck, Mishcon de Reya and DWF land on my desk all in one day. The scammers’ lawyers bleat loudly about their “poor” clients’ reputations.

Every pension scam starts with a negligent transfer

But the ceding providers are just as bad: their lawyers think it is fine to facilitate financial crime. Here’s an extract from recent letter from one of them:

“You state you have “hard evidence” that our customers “have suffered serious loss because of our negligence”. You have not provided any such evidence. Please therefore produce such ‘hard evidence’ by return.”

This lawyer went on to request evidence that the provider ought to have known that the receiving scheme in

question was a scam. She went on to state that my allegations were “wholly unfounded” and to demand that I take down this blog:

But this pension provider has given me no reason to take the blog down – and no justification for the claim that the firm is “innocent” of handing over victims’ pensions to obvious scammers. Back in 2010, the Pensions Regulator warned providers about transferring pension funds to scams:

“Any administrator who simply ticks a box and allows a transfer post July 2010 is failing in their duty as a trustee and as such are liable to compensate the beneficiary.”

But the providers have studiously ignored the regulator’s warning for nine years. And thousands have lost their pensions as a result of this sickening negligence.

Transferring pensions to scammers

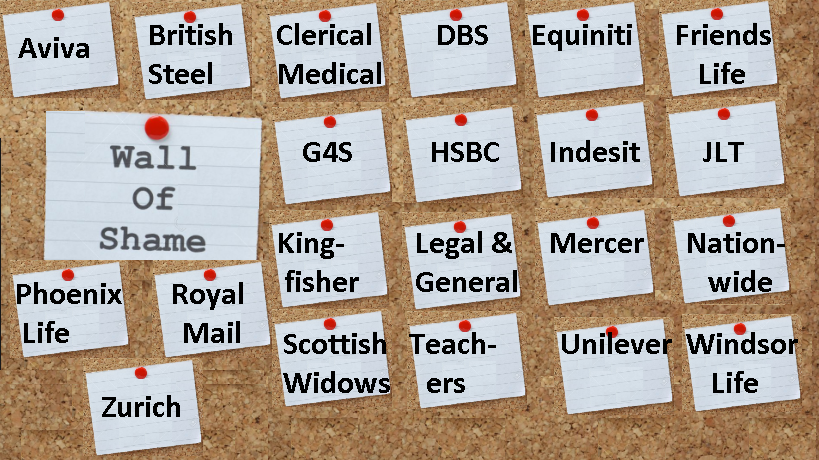

Here is an “A to Z” of the pensions industry’s negligence in handing over thousands of pensions in defiance of numerous warnings since 2010. Note: to my knowledge not a single administrator has voluntarily compensated their victims – and all have emphatically denied they did anything wrong.

Transferring pensions to scammers – the ABC of shame

Aviva: Second only to Aegon in our list of shame, Aviva transferred numerous pensions from October 2013 onwards. This was well after the Pensions Regulator’s “Scorpion” warning. The largest of these was £258,684.05 at the request of well-known scammer Stephen Ward of Premier Pension Solutions. Ward had been behind the £27 million Ark liberation scam in 2010. On 21st January 2015, Aviva’s Robert Palmer told me they needed no help or advice with avoiding negligent transfers to obvious scams. One month later, Aviva handed over £23,500 to the GFS scam.

British Steel: Long before the much-publicised handing over of multiple members to scammers in 2018, British Steel was handing over pensions to the Hong Kong GFS QROPS scam in 2014 . Mainly advised by serial scammer David Vilka of Square Mile International Financial Services in the Czech Republic, the GFS scam invested hundreds of victims’ funds in UCIS funds such as Blackmore Global.

Clerical Medical: Another disgraceful firm with a long history of handing over pensions to Ark, Capita Oak, Westminster and GFS in 2014.

This A to Z of shame goes on and on – and includes all the big names (who should have known better):

ALL PENSION SCAMS START WITH A TRANSFER BY A CEDING PENSION PROVIDER.

It is interesting that PSIG chose three particular providers to give their answers to the questionnaire sent out: XPS Pensions Group, Phoenix Life Assurance Company and Standard Life Assurance Company. I have no doubt they chose these three providers because of their extensive first-hand expertise at facilitating financial crime. In the Capita Oak and Westminster scams – distributed and administered by serial scammers XXXX and Stephen Ward – and now under investigation by the Serious Fraud Office – Phoenix Life and Standard Life handed over dozens of pensions to the scammers. In Phoenix Life’s case, the total came to nearly half a million pounds’ worth, and in Standard Life’s case it was well over one million.

While there is, of course, substantial hard evidence that both the Pensions Regulator (formerly OPRA) and HMRC had been giving the industry plenty of warnings about scams long before the Scorpion Campaign was published on Valentine’s Day in 2013, it is also true that providers such as Phoenix Life, Standard Life – and other favourite financial crime facilitators such as Aegon, Friends Life, Legal & General, Prudential, Royal London, Scottish Life and Scottish Widows – carried on handing over millions to the scammers well into 2014, 2015 and beyond. And, in fact, they are still at it today.

The “Key Findings” do throw up some interesting facts:

“Information on scams is not readily available at an organisational level”.

Seriously? Don’t these organisations know how to do research? Do they really not know what to look for? They’ve had enough experience over the years – and have had enough examples of spending vast amounts of time trying to cook up reasons to deny complaints against their incompetence for handing over pensions to scammers – to write a whole encyclopedia about scams.

Organisations (such as Phoenix Life and Standard Life) could try talking to TPAS, or tPR, or the FCA, or the SFO, or Dalriada Trustees, or regulators in Malta, the IoM, Gibraltar, Dubai or Hong Kong. Or some of the thousands of victims – who have lost their pensions due to the incompetence and callousness of the ceding providers – who would readily fill in the blanks. There really is no shortage of readily-available, free information. They just need to take the time and trouble to ask for it. It really isn’t difficult. They just have to put their box-ticking pencils down for a few minutes.

“The Scams Code is seen as a good basis for due diligence”

I agree – it is really great. But it is also 78 pages long. Few people have to the time to read, understand or remember such long documents (with too many long words and not enough pictures). What would be helpful would be to get a few of the worst offenders: Aegon, Aviva, Friends Life, Legal & General, Phoenix, Prudential, Royal London, Scottish Life, Scottish Widows, Standard Life and Zurich, in a room at the same time – and bang their heads together. And threaten them that if they don’t get their acts together and stop handing over pensions to the scammers, they will be made to read and memorise the 78-page Scams Code and recite it every morning before coffee break. Twice. Then snap all their box-ticking pencils in half, and JOB DONE! It really isn’t rocket science – there are usually some hints which are as subtle as a brick, such as: the sponsoring employer doesn’t exist; or the member lives in Scunthorpe and is transferring to a scheme whose sponsoring employer is based in Cyprus. Or Hong Kong. Now, I know there was a bit of a hiccup with the Royal London v Hughes case when Justice Morgan overturned the Ombudsman’s determination. But dear old Hughes had probably had a few Babychams too many – and it had slipped his mind that the law is supposed to be about justice and common sense. And that just because a particular piece of legislation has been written by an ass, it doesn’t have to be interpreted with stupidity.

“Significant time and effort goes into protecting members from scams”

This, of course, may be true. I only get to see the cases where the negligent ceding providers dohand over the pensions to the scammers. I rarely get to see the ones that have a narrow escape. But what worries me is that I am in the process of making complaints to the ceding providers who have handed over pensions to the scammers, and not a single one of them thinks they have done anything wrong. So, if they do spend “significant time and effort” doing the protecting bit, how come so many of them still fail so badly? And then try to deny they failed. These providers spend very significant amounts of time and effort writing long, boring letters about how they did nothing wrong – letters which must have taken them at least an hour to write. And yet they won’t spent two minutes checking – and stopping – transfers to obvious scams.

“The more detailed the due diligence, the more suspicious traits are identified”

I am a bit suspicious that this indicates a touch of porky pies here. I’ve never seen any evidence of ANY due diligence by the ceding providers. A bloke at Aviva once told me that they spent thousands on research and due diligence – but I see no evidence of it. The problem is, the ceding providers don’t know what they don’t know. And, to coin one of my favourite phrases: “they don’t know the questions to ask, and even if they did then they wouldn’t understand the answers”.

Interestingly, if – instead of repeatedly spending hours denying they did anything wrong when they handed over millions of pounds’ worth of pensions to the scammers – they spent some time talking to me and the victims trying to learn what went wrong and what due diligence should have gone into preventing a dodgy transfer, they might learn how to stop failing so badly.

SIPPS (including international SIPPS) are the vehicle of choice by scammers

Agreed. But the scammers still love the good old QROPS. But whether it is a SIPPS or a QROPS – both of which are just “wrappers” at the end of the day, it is about what goes inside the wrappers. Where the scammers make their money is in the kickbacks: 8% on the pointless, expensive insurance bond from OMI, SEB, Generali, RL360, Friends Provident etc., and then more fat commissions on the expensive funds or structured notes.

“Quality of adviser tops the list of practitioner concerns, with member awareness a close second”

And hereby lies one of the main problems: ceding providers don’t know who the good guys are and who the bad guys are. And that is because they don’t ask. And they don’t learn from their mistakes when they get it wrong. And they don’t care when they hand the pensions over to the bad guys and their former member is now financially ruined and contemplating suicide. Instead of trying to use their appalling mistakes to improve their performance and understand what “quality” actually means, and how to tell the difference between good and bad quality, they only care about avoiding responsibility for their own failings.

The problem about “member awareness” is that most people assume their ceding provider will do some sort of due diligence. They think that words like “Phoenix Life”, “Prudential” and “Standard Life” convey some sort of professionalism or duty of care. Most members are simply unaware of the appalling track record of these providers – and the extraordinary and exhaustive lengths to which they will go to avoid being brought to justice for their negligence and laziness.

“Sharing of intelligence would help avoid duplication of effort”

Oh, how heartily I agree! I remember a year or so ago, I shared some intelligence and a few beers with a nice chap from Scottish Widows. We met at one of Andy Agathangelou’s symposiums in London – the subject of which was pension scams. The Pensions Regulator was there, Dalriada Trustees were there, Pension Bee were there, lots of interested parties were there (including an American insurer from Singapore), and a couple of victims. I gave a joint presentation with one of the victims who described how he had been scammed and how his provider had handed over his pension so easily – well after the Scorpion watershed. The nice chap from Scottish Widows asked the victim why he hadn’t called the Police. The victim replied: “I am the Police”.

It was very telling that the room wasn’t full of delegates from Aviva, Phoenix Life, Prudential, Standard Life etc. None of them were interested.

Not a single provider has ever phoned me up to ask for advice, or to arrange to speak to some victims to learn something about how they were scammed and how and why their ceding providers had failed them so badly. There are so many victims all over the UK and the rest of the world. And what they all share is a passion to try to prevent other people from being scammed by the bad guys and failed by the bad pension providers. So this invaluable intelligence is freely available.

Until and unless the providers develop a conscience, they are going to continue to fuel the pension scam industry – and nothing will change. And the 79-page code might just as well be consigned to the bathrooms of Aegon, Aviva, Friends Life, Legal & General, Phoenix, Prudential, Royal London, Scottish Life, Scottish Widows, Standard Life and Zurich.

I “borrowed” this blog from my Twitter friend in Singapore who clearly understands and cares about investment scams – and the inability of the inept authorities to do anything about them. This is true not just in Singapore but throughout the world – particularly the UK, the Isle of Man, Gibraltar, the Cayman Islands, Guernsey, Ireland, Dubai, and Hong Kong.

I could not improve upon his excellent blog, but I have put some comments in red in the body of the text (with apologies to Lee!).

This is a story about how scammers have used the loopholes within the law to fleece hundreds of millions of dollars (and pounds and Euros in other jurisdictions) from an unsuspecting public. Many of whom are retirees and young people venturing into alternative investments for the first time in their lives.

In Singapore, there are two primary agencies that are set up to ensure a safe investment environment for its people. The Monetary Authority of Singapore (MAS) that regulates the financial industry and the Commercial Affairs Department (CAD) of the Singapore Police Force that investigates commercial crime and Fraud.

Just wanted to add a few more: chia seeds, eucalyptus plantations, truffle trees, forex trading, life assurance policies, football betting, property loans, rubbish recycling, litigation funding, timeshares, films, claims management companies etc.

In support of innovation (Lee uses the word “innovation” – but I would have used the word “opportunism”) in the financial industry, Alternative Investment Offers have been allowed to thrive. Non-traditional Products are being offered to the lay public, advertised widely on social media and even in the mainstream media with barely any restrictions. (In the UK, we would refer to many of these as UCIS – unregulated collective investment schemes – which are illegal to promote to retail investors). Many vendors of these make wild claims of double-digit percentage returns per annum, sometimes coupled with apparent full capital protection that targetted investors would just swallow wholesale.

These companies are not regulated by MAS and will often be listed as such in the MAS-issued Investor Alert List. But being on the Investor Alert List simply means Caveat Emptor … nothing more. Legitimate companies, as well as unscrupulous ones, are similarly listed there without distinction. So in most cases, the attractive returns and false assurance of safety are just too irresistible to the average investors who would be pulled in by the hundreds, if not thousands. I reckon few people ever think to look at the MAS website – just as few ever look at the FCA website where well-hidden warnings lurk deep below the surface.

While not all Alternative Investments are dodgy, many of them are because the current law offers a fairly wide window (between 3 to 8 years) for them to operate before the law catches up. Why? Because the law enforcement agency that investigates fraud only starts to investigate after many victims have reported their loss. There are victims who do not report because of fear, because of embarrassment, because of unrealistic, hopeful optimism and a variety of other reasons so by the time CAD gets involved, it would have added more years and more new victims. A lot more people, sadly, would have been hurt by then. This is the most significant factor in stopping financial fraud – if the first whistle were to prompt action by the authorities, more victims could be prevented. The feet of clay by regulators and law enforcers help the scammers and facilitate the crimes.

Ponzi schemes are chief among these and as with all Ponzis, the early investors are taken in by the promised high returns being achieved. This pool of satisfied investors will go on to sink in additional funds. But more than that, they are often trotted out on stage at investment seminars to be the best spokespersons for their “safe and profitable” investments. Some are even recruited to be sub-agents who earn referral commissions.

A very common scam I see over recent years involves companies that may own some land in a distant country, directly or indirectly via their selected “Developer Partners” who have cleared their “rigorous” due diligence process and deemed safe. Money is borrowed from the lay public by an intermediary set up for that specific fundraising purpose. This intermediary is supposed to channel the funds out to the said Developers for the purpose of infrastructure development or some construction activities on the property. In return, the intermediary company, freshly created, probably a limited liability entity registered in some opaque tax-free haven, signs an IOU agreement with the investor detailing scheduled repayments of interests and full capital at the end of 2 or 3 or 4-year terms. He’s just described Dolphin Trust and similar investment “loan-note” scams perfectly.

The IOU agreement or promissory note does not accord the investors (or more accurately the lenders), any say on how the funds are utilised. There is also nothing to stop these unscrupulous vendors from using that same plot of land as their “collateral” to draw in funds from other investors in other markets.

Theoretically, that same piece of land could be used multiple times to borrow new money as long as the investors were not aware of it and had no legal title on that property. The number of times this “asset” is leveraged is limited only to the diabolical ingenuity of those vendors and the trusting innocence of an investing client pool. Am getting a bit worried now, as I think some of the scammers – who hadn’t already thought of this – might be getting very excited!

Other fundraising schemes can be created… perhaps through the issuance of minibonds in countries like the UK or in Europe. Or through commercial paper described as Development Funds that pay generous coupon rates over medium term, offered to selected high net worth clients. (And low-net-worth clients – the scammers aren’t fussy!).

Different company names are formed but the directors may be the same. The product brief is almost always similar and the advertising media material professionally done and is always flashy. Invariably these vendors will hold charity events and engage media celebrities or host politicians to lend credibility to their cause. They would list fake awards and renowned organisations as their business partners on their websites. All these with the sole intent of creating an image of legitimacy. This perfectly describes Phillip Nunn and his Blackmore Global investment scams – promoted by David Vilka.

Sometimes they may even attempt to raise public funds via a back door listing through an acquisition of a public listed entity that had fallen under judicial management.

Who are these people who are capable of such an elaborate scheme that spans international borders? Will the law catch up with them before they escape with their ill-gotten loot? Will justice be served in time and make an example of how fraud should not be excused as business failure?

Alas, only time will tell. Lee doesn’t seem optimistic. And I most certainly am not. The scammers make far too much money from such investment scams – and pension savers are ridiculously easy targets. The cold-calling ban will have negligible effect, and the ceding pension providers will keep on keeping on handing over pensions to the scammers willy-nilly.

I must admit, I had always been under the impression that regulation and law enforcement in Singapore were superb. But reading Lee’s blog, and learning how UOB bank has stolen £ millions from one customer, I think Singapore is probably as hopeless at challenging scams and financial fraud as the rest of the World.

BREXIT is the question on everybody’s lips at the moment. BREXIT: will we? won´t we? deal? no deal? So many unanswered questions and so much scaremongering. We would like to offer some helpful words and hopefully protect you from making rash decisions. This could help you to safeguard your pension. Many scammers are trying to cash in on Brexit – make sure sure you’re not their next victim.

Remember I am not a financial adviser. I am a blogger, and I write about financial crime. I provide information about past scams and on how to avoid falling victim to new scams – especially pension scams. The words I write are aimed to help you safeguard your pension from the many offshore scammers.

So, Expats, what does Brexit mean for your pension rights? The short answer is that we really do not know! There are currently lots of “coulds” and “mights” being thrown around, but no certainties. And herein lies the risk that you and your pension could fall victim to a scam with all this scaremongering.

Firstly, despite Spectrum IFA advertising themselves as “international financial advisers”, with some digging we were able to find out that they DO NOT in fact have an investment licence. This means they are not legally allowed to advise on pensions or investments. Secondly, they scored rather poorly on the qualified and registered percentage too. Out of the 16 advisers we checked up on, only four were registered with the appropriate institutes. The rest came up red – meaning the institute had no record of them.

Worrying isn´t it? Offshore companies can try to claim they are international financial advisers, but actually be unregulated and unqualified to carry out the very service they offer! The “advisory” firms have flash websites, and some have several offices around Europe and beyond. Their PR is great at scaremongering expats about their pension investments in the lead up to Brexit.

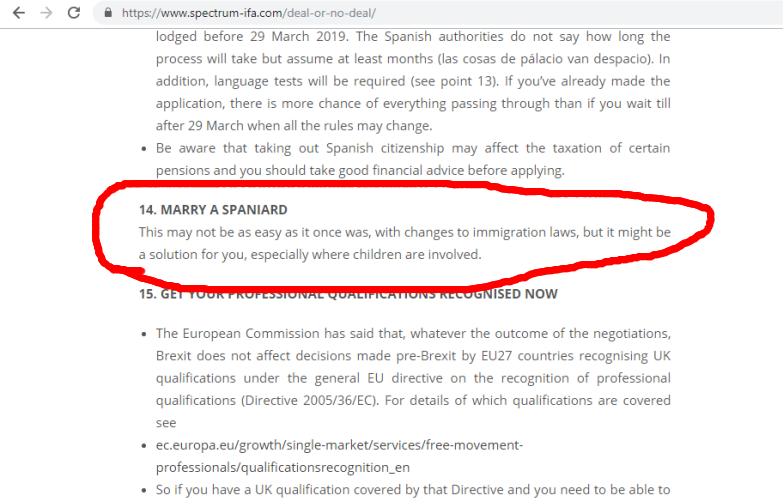

In Spectrum’s ´Deal or no deal´ article number 14, they suggest you marry a Spaniard in order to prepare for Brexit. I´m not sure about you, but I feel that getting hitched to a native to be able to stay in Spain is a pretty drastic measure and definitely more than a little illegal.

Spectrum IFA is just one example of a firm that probably ought to be given a wide berth when transferring your precious pension fund offshore. Safeguard your pension by avoiding unregulated and unqualified firms like this one.

********

It may seem daunting when you read that your UK pension could be subjected to extra taxes if we leave the EU on a no-deal basis. You may be thinking that you should transfer into a QROPS quickly, to save on these taxes. But what you really need to know is that a QROPS is not without punitive costs of its own. They can be expensive and unless you have a good lump sum to transfer you could see a huge chunk of your pension pot taken in transfer and set-up fees anyway! Potentially making you worse off.

Unfortunately, until we make a deal or actually go through with Brexit, nothing is very clear for expats. Which leaves us in an uncertain time and situation. This, I understand, may be daunting for many people, but I urge you to take a deep breath before considering any speedy offshore pension transfers. Thousands of people – especially those who have already fallen victim to scammers such as Continental Wealth Management – would give you exactly the same urgent advice.

If you do want to transfer your pension, please heed this advice to safeguard your pension:

We did a series of blogs last year on offshore companies and their advisers. The results were extremely worrying. Aside from their blatant disregard for the necessity of these qualifications – due to being offshore – the number of unqualified advisers offshore was cause for serious concern. Many of the firms had not one single qualified and registered adviser on their team.

A reputable firm will have a fact-find procedure, and adhere to a client’s risk profile.

A reputable firm will have compliance procedure.

A reputable firm will have clear and consistent explanations and justifications for the use of insurance bonds.

Where will your funds be invested, and how will you know if this is in line with your risk profile?

A pension fund should be placed into a low-medium risk investment.

Scammers tend to go for high-risk, professional-investor-only investments as they offer them the best commissions. But a pension fund should have more protection than this. Avoid investments that involve structured notes (like CWM´s Blue Chip notes), UCIS funds (like Blackmore Global), in-house funds, non-standard assets and any ongoing commission-paying investments.

Insurance bonds – often used by scammers – are usually an unnecessary double wrapper on your fund, that costs you more in fees and charges than a straightforward platform, lining the pockets of the scammers – but making your fund smaller.

How much will the fees and charges be? Remember NO pension transfer is free.

Legitimate firms will normally have a small transfer charge and a small annual fee.

Scammers will often be vague about fees and charges, and avoid giving you a straight answer so they can cover up the true figures. These hidden figures can see your pension fund decrease by 25% or even more in some cases.

A reputable firm should offer you regular updates on the progress of your fund.

You should receive an annual review and a quarterly update showing the fees, charges and growth of your fund.

If your new firm and adviser fail to do this, alarm bells should ring loudly.

Finally, a reputable company will publish evidence to show records of complaints made, rejected or upheld and redress paid.

If the adviser cannot show you all this information, do not trust them.

If it all sounds to good to be true, it probably is – RUN!

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “scammers are criminals“. However, the sad truth is that most of them have not been prosecuted or jailed.

The vast majority of the well-known pension scammers are still roaming free, busy thinking up yet more life-destroying schemes to make them rich and the victims poor. Whilst the scammers enjoy champagne this New Year’s Eve, many victims will be worrying themselves sick about their bleak financial future.

The Pensions Regulator, the Serious Fraud Office, the Insolvency Service, crime enforcement agencies and courts all seem to drag their feet when it comes to actually bringing charges against these criminals. Yet we see people being locked up for renting out caravans to help vulnerable homeless families! I would love it if this was a short and sweet blog, with many happy endings. But, alas, the scams are plentiful and the victims are left uncompensated for their losses.

Let’s have a quick round up of where we are with the scams and scammers. And remember: all the thousands of victims want to see the scammers sent to jail and the keys thrown away so they can’t ruin any more innocent people’s lives.

5G Futures

5G Futures: in May 2013 Garry John Williams and Susan Lynn Huxley were suspended as trustees of the 5G Futures pension scheme, and from trust schemes in general. Pi Consulting was appointed as the new trustee by the Pensions Regulator.

About 400 people had invested a total of £20m into the 5G Futures scheme – which was invested in high-risk, illiquid off-shore investments, with insufficient diversification making them completely unsuitable for pension scheme investments. There was no due diligence exercised by Williams and Huxley – and the scheme records were a mess.

The scheme operated pension liberation through ‘loans’ to members. Williams and Huxley were found to have taken very high commissions on the investments – taking nearly £900,00 in one year alone.

One of the most worrying things, however, is that the pension scammers don’t just leave the pensions industry and dedicate themselves to helping their many distressed victims – they start up all over again:

Stephen Ward: (this will not be the last time you hear this name in this blog) was the mastermind behind this scam (dating back to 2010). It was his first known scam – but by no means his last one. What is left of the Ark fund, stands still frozen, in the hands of Dalriada Trustees, who continue to take their yearly costs and fees from what little is left. Dalriada has done nothing to ensure the scammers are prosecuted – saying it is “not within their remit”. The victims of the Ark scam also have the heavy hand of HMRC hanging over them. And let us not forget that it was HMRC who happily registered this scam and failed to withdraw the registration when they discovered that Stephen Ward was operating pension liberation fraud.

Dalriada has never reported Stephen Ward to the police as it is not “within their remit” to ensure the scammers are prosecuted.

In 2018 we saw Stephen Ward being banned from acting as a pension trustee. Eight years after his first scam, he has still not been imprisoned for the millions of pounds’ worth of life savings he has destroyed and the thousands of lives he has ruined.

Other prominent figures in the Ark scam were Julian Hanson – who went on to play a key role in the Friendly Pensions scam; George Frost who went on to operate a new pension liberation scam using truffle trees as investments; Andrew Isles who went on to sell his accountancy business, Isles and Storer to LB Group; Peter Moat of Blu Debt Management who went on to operate the Fast Pensions scam. None of these scammers has ever been convicted or jailed.

Axiom

Another pension liberation scam, which saw victims with HMRC tax demands of 55%. Rex Ashcroft of Wealth Protection International was one of the main introducers of this scam. According to his Linkedin profile, he offers business development strategy planning for the UK, Spain, Portugal and France. He also offers “day-to-day application of wealth protection strategies”. Ashcroft lied to Axiom victims telling them they could access part of their pensions and not pay tax on the cash they took out.

David Vilka, Phillip Nunn and Patrick McCreesh have never been convicted or jailed. Blackmore Global Group is still being promoted by Phillip Nunn! Nunn and McCreesh had been the main lead generators in the Capita Oak scam – earning nearly £1 million in the process.

This was another of Stephen Ward´s scams – on which he worked closely with his pensions lawyer Alan Fowler (ex Stevens and Bolton Solicitors) and his sidekick Bill Perkins. Ward carried out the transfer administration for this scam which was mainly operated by XXXX XXXX who offered victims 5% Thurlston “loans”. Over 300 victims are facing the partial or total loss of their pensions and are also now being pursued by HMRC for tax liabilities on the “loans”.

Capita Oak – like Ark – was placed in the hands of Dalriada Trustees. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward, Alan Fowler, Bill Perkins and XXXX XXXX have never been convicted or jailed (although XXXX XXXX is under investigation by the Serious Fraud Office).

Stephen Ward’s firm Premier Pension Solutions (in Moraira, Spain) was the “sister” firm of Continental Wealth Management, run by scammer Darren Kirby. This was one of the biggest single scams – known as CWM – with around 1,000 victims losing part or all of their life savings. Other scammers involved were Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway.

This scam was promoted by cold-calling victims and promising unrealistically high returns and “capital protection”. Darren Kirby and Anthony Downs used the victims’ funds to invest in totally unsuitable, high-risk, fixed-term structured notes. This scam saw huge commissions paid by the life offices – Old Mutual International, SEB, and Generali – as well as by the structured note providers: Leonteq, Commerzbank, Royal Bank of Canada, and BNP Paribas to this unregulated firm. Let us not forget that this was without question financial crime and was facilitated by the life offices.

Old Mutual International, run by ex IoM regulator Peter Kenny, was the leading life office which facilitated the CWM scam. Generali and SEB also routinely accepted business from these known scammers and unlicensed advisers.

Stephen Ward, Darren Kirby, Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway have never been convicted or jailed.

James Hay and Suffolk Life were accepting Elysian shares for liberation purposes

Another Stephen Ward creation which was operating 80% liberation with the full cooperation of the SIPPS providers James Hay and Suffolk Life. The SIPPS providers and the victims could face tax charges of up to £20 million from HMRC.

Despite clear evidence that Stephen Ward pushed this scam in emails to Alan Fowler and Bill Perkins, neither Ward nor Fowler nor Perkins have ever been prosecuted or jailed.

A New Zealand QROPS scam with Marazion pension loans

When Ark got shut down, Stephen Ward went straight to New Zealand to set up his next pension liberation scam with Simon Swallow of Charter Square. A further 300 victims were scammed out of over £10 million and conned into Marazion “loans” AND locked into the Evergreen scheme for five years. After the five years victims were told: ´Despite our best efforts, Evergreen has not been as successful as we had originally hoped.´ Evergreen was wound up April 208.

This scam was promoted by Darren Kirby’s Continental Wealth Management which cold called the victims.

Stephen Ward, Darren Kirby, and Simon Swallow have never been convicted or jailed.

It was determined that there is no doubt this was a scam.

Peter and Sara Moat and their accomplices have never been convicted or jailed.

Friendly Pensions Limited (FPL)

Back in January of 2018, the Pensions Regulator asked the High Court to act on their behalf in the Friendly Pensions matter. Scammers: David Austin, Susan Dalton, Alan Barratt and Julian Hanson (also involved in ARK) were ordered to pay back £13.7 million they took from their victims and banned from being pension trustees. However, Dalriada the independent trustee appointed by TPR to take over the running of the schemes, is in charge of confiscating the scammers’ assets for the benefit of their victims. (Who knows how long this could take: how long is a piece of string?) As yet, no compensation has been offered to the victims.

David Austin, Susan Dalton, Alan Barratt and Julian Hanson and their accomplices have never been convicted or jailed. However, there have recently been some arrests – so let us hope this results in maximum sentences.

Two bogus “occupational pension schemes” set up for pension liberation fraud by Stephen Ward after the Evergreen QROPS scam hit the rocks (when HMRC removed Evergreen from the QROPS list). Victims have no idea where or how their pensions are invested. The pensions are allegedly invested in “The Treasury Plus Fund” (whatever that might be – and it is not likely to be anything good) and the trustee is Ward’s bogus trustee firm Dorrixo Alliance.

Nobody knows the total aggregate value of lost pensions and tax liabilities Ward has caused – we hazard a guess at a figure in the region of £100 million +.

Another double act by Stephen Ward and XXXX XXXX. This was the “sister” scheme to Capita Oak. Ward did the transfer administration – from safe, well-known and regulated pension providers to this bogus occupational scheme run by XXXX.

Neither Stephen Ward nor XXXX XXXX has ever been convicted or jailed.

Another pension liberation scam – placed in the hands of Dalriada Trustees by the Pensions Regulator.

Incartus was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported the scammers to the police as it is not “within their remit” to ensure the scammers are prosecuted.

None of the Incartus or Bluefin trustees scammers has ever been convicted or jailed.

£11.9 million worth of transfers were made, with the victims receiving approximately 50% of their pension as a loan and the promise of the rest being invested into a high-interest generating SIPPS. The loans were made from the pensions and therefore the victims have the usual HMRC tax demand letters. Further to the victims’ misery, the other 50% of the funds was not invested as promised. Most of the funds were swallowed by high commissions paid to the scammers.

None of the KJK Investments/G Loans scammers has ever been convicted or jailed.

Another of Stephen Ward’s many pension scams, this one was courtesy of his bogus pension trustee firm Dorrixo Alliance, his accomplice Gary Barlow at Gerard Associates, and introducers at Viva Costa International. Like Ward´s other scams, London Quantum scam was never set up for the benefit of the victims, but in the interests of Stephen Ward and his team of scammers to earn the maximum amount of commission out of the toxic, illiquid, high-risk investments.

The London Quantum scam is now in the hands of Dalriada Trustees.

London Quantum – like Ark, Capita Oak and Fast Pensions – was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward and Gary Barlow have never been convicted or jailed.

This pension liberation scam dating back to 2013 and 2014, involved around £1m of victims pension funds. Anthony Locke, was sentenced to a five-year jail term and Ray King, 54, who was employed by Lock, was given a three-year jail sentence.

It is great that these two crooks received jail terms, however, they are relatively “small fry” in comparison to the other serial scammers who are still walking free! The question remains: why have two minor players such as Locke and King been convicted and jailed while the “big fish” remain free to keep on scamming?

116 victims were scammed out of their pensions by James Lau of FCA-regulated Wightman Fletcher McCabe. Victims were assured the loans they were given did not come from their pension funds and would not be taxable by HMRC. The trustees of the scheme – Peter Bradley and Andrew Meeson (both ex HMRC) of Tudor Capital Management – were jailed for eight years for cheating the Public Revenue. James Lau is currently under criminal investigation by the Insolvency Service. The victims are awaiting a verdict on whether they will still have to pay the tax penalties.

James Lau has not yet been convicted or jailed – although he is clearly a wanted man.

This scam was facilitated by STM Fidecs in Gibraltar – one of Europe’s biggest QROPS providers. The regulator did order Deloittes to carry out an inspection into STM Fidecs’ books, but no action was taken against STM Fidecs for their part in this scam.

STM Fidecs accepted transfers into the QROPS by UK-resident victims “advised” by XXXX XXXX – even though he was not licensed to give financial advice. And then XXXX’s clients were 100% invested in XXXX’s own fund.

XXXX XXXX has not yet been convicted or jailed – although he is clearly under investigation by the Serious Fraud Office.

Another of the schemes under investigation by the SFO. This liberation scam with more than £3 million worth of (now worthless) investments was registered and administered by Stephen Ward.

Windsor Pensions

A no-frills pension liberation scam run by Florida-based Steve Pimlott. This scam has been going on for years and there is no sign of any let up – despite the fact that the regulators and ombudsman are well aware of Pimlott’s modus operandi. Pimlott doesn’t bother with any attempt to conceal the loans with fancy “loans” or complex mechanisms to try to “distance” the liberation from the pension transfer. He uses QROPS and a fraudulently-set-up bank account in the Isle of Man (of course!). HMRC catches many of the victims and charges them 55% tax on the liberated amount. Pimlott charges around 15% for the liberation.

Steve Pimlott has not yet been convicted or jailed

What a sorry state of affairs that out of all the pension schemes I have mentioned here, only one of them has seen the scammers jailed. Serial scammers like Stephen Ward and XXXX XXXX seem to slip the noose of justice again and again.

International Adviser really can’t make up its mind whether it is organising a piss-up in a brewery, a news roundup carefully slewed in favour sponsors Old Mutual International, or a marketing machine. I read with interest the recent IA Industry Most Influential Top 100 described by IA thus: “we at International Adviser decided to shine a light on the movers and shakers that have helped this industry get to where it is today”.

But where exactly is the industry today? And have the so-called top 100 moved and shaken the industry in a helpful way or a detrimental way? To find out, why don’t we have a look at a few of the “influencers”. To get the measure of them, let’s put them into a game of “Have I Got News For You”:

Bob Pain in the chair as quiz master. A bloke who ran Cayman Islands-based Investors Trust until recently appointed chair of the Association of International Life Offices, the trade body for international life offices. During his 35 years of experience in financial services, he facilitated the scam run by Phillip Nunn of Blackmore Global and David Vilka of Square Mile International Financial Services. Investors Trust accepted over 1,000 investments into illegal UCIS funds for UK-based victims scammed into QROPS with Integrated Capabilities and Harbour (now STM).

As Captain of the Navel Team, let’s have dashing Tim Searle – Chairman of Dubai-based Globaleye. With his eight-year Naval history, he should make an ideal leader and would come in particularly useful in the event of icebergs, torpedos or sharks.

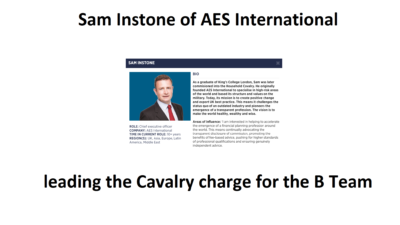

Captain of the Army Team I nominate as Sam Instone of AES International. His experience as an Army officer should give him the leadership skills to oppose the Navel Team. Sam’s track record as the “enemy of traditional financial services” should give him the basis for a sound battle plan.

On the Army Team, we’ll have international wealth and regulatory specialist, Phil Billingham. Phil must be utterly disgusted with the likes of Stephen Ward (another fully-qualified adviser) messing up the reputation of the profession by running a long series of pension scams and ruining thousands of lives.

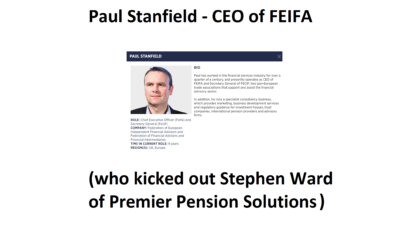

And the final member of the Army team will be Paul Stanfield, CEO of FEIFA (Federation of European Independent Financial Advisers). Another real gentleman – and handsome to boot – and one who understands the importance of outlawing scammers. Several years ago he excommunicated Stephen Ward of Premier Pension Solutions from FEIFA to loud cheers from victims and industry professionals alike. (My only gripe with him would be that he still hasn’t kicked out Square Mile Financial Services run by scammers John Ferguson and David Vilka).

On the Navel Team we’ll have Geraint Davies of Montfort International – an expert IFA specialising in international financial services, and Roger Berry of Concept Group Trustees in Guernsey. These two chaps also have, between them, extensive experience of Stephen Ward in their own ways and will, no doubt, have much to talk about.

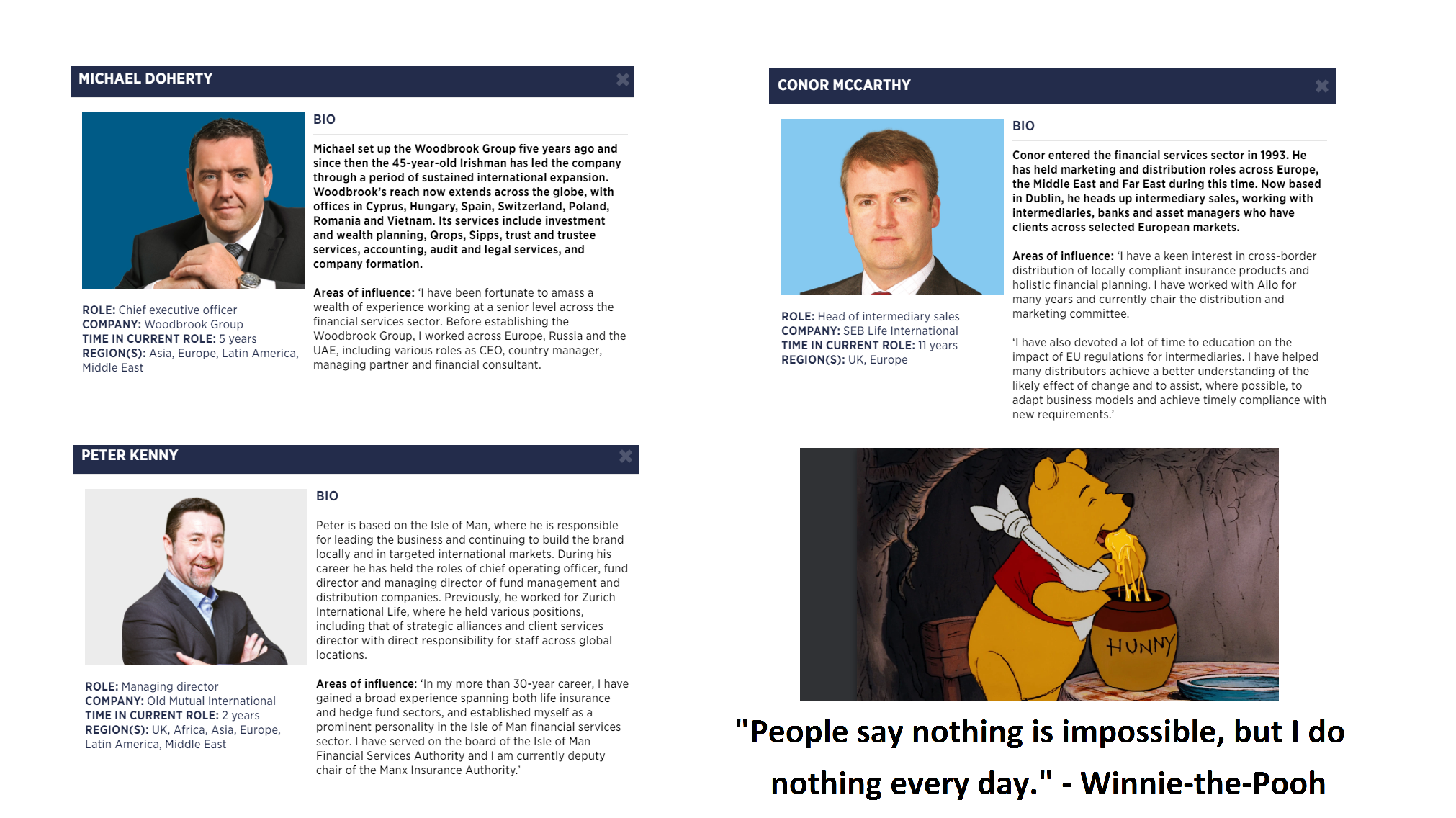

The contest will be to spot the “odd one out”: Michael Doherty of Woodbrook Group, Conor McCarthy of SEB, Peter Kenny of OMI and Winnie-the-Pooh.

Tim Searle: “They’re all Irish, except Winnie-the-Pooh who’s English?”

Geraint Davies: “They all hate Angie except Winnie-the-Pooh who’s never heard of her?”

Roger Berry: “They all love Angie except Winnie-the-Pooh who’s never heard of her?”

Sam Instone: “They’ve all got names that end in Y except Winnie-the-Pooh?”

Phil Billingham: “They’re all involved in money except Winnie-the-Pooh who’s involved in honey?”

Paul Stanfield: “None of them have applied to be members of FEIFA except Winnie-the-Pooh?”

Bob Pain: “No, you’re all wrong. The answer is Peter Kenny of OMI. The other three have been doing “nothing”: Michael Doherty was employing ex CWM scammers Dean Stogsdill and Neil Hathaway (known as Dog Kill and Hadaway) but claimed he was paying them nothing; Conor McCarthy of SEB has been asked numerous times for his comments on why SEB allowed the scammers at CWM to invest most of their victims’ funds in toxic structured notes, but McCarthy is saying nothing and won’t reply; and Winnie-the-Pool is doing nothing all the time.

The odd one out is Peter Kenny who is doing “something” and is suing Leonteq for the £94 million worth of fraudulent structured notes they sold to OMI.

Integrated Capabilities – a Trust Company based in Malta have created their own Pension Scheme – Azure Pensions. On the face of it, however, the management team do not appear to have learned anything from their previous experience with Optimus Retirement Benefit Scheme No.1 and their association with David Vilka of Square Mile International Financial. It appears they have now teamed up with some very dubious friends – the result of which is very likely to create more victims of UK pension scams.

I AM GRATEFUL TO STEVE – ONE OF THE BLACKMORE GLOBAL/DAVID VILKA VICTIMS – FOR RE-WRITING THIS BLOG AT THE REQUEST OF INTEGRATED CAPABILITIES’ LAWYER.

The Azure website states: “We believe that trust is built and earned. As such we have an ingrained and sustained desire to develop long-term relationships with our clients”. These are just words and words are easy. It’s what you do that counts.

In 2015, the Optimus scheme started out with 26 members and by the end finished up with 1,176 – that’s a gain of almost 100 new members per month! I was one such member conned into transferring my pension by fraudulent misrepresentations made by David Vilka of Square Mile Financial Services.

This new pension arrangement locked me in for 10 years – definitely a “long-term relationship” – giving all parties the opportunity to drain my pension dry in fees. Credit where credit is due, however. Once I discovered I was in a scam, the director Andy Dawson (bottom row, 3rd from the left) did make an extraordinary effort not only to redeem the investments but successfully persuaded most parties to waive their early exit penalties and refund their fees. Only the greedy Symphony Fund chose to keep the penalties and that’s after mysteriously dropping in value 30% just before redemption. Thanks to Andy Dawson and his team, I did manage to get back 92% of my pension. But the BIG QUESTION is what has happened to the other 1,100+ members? It is inconceivable I was the only one transferred into this scheme via Vilka et al.

Another claim made by Azure Pensions is: “Our people are highly experienced, knowledgeable and motivated to do their utmost to ensure that they deliver a superior, professional and hassle-free service.” But this firm, and the people in it, have a history of working with scammers and investing members’ retirement funds in investment scams such as Phillip Nunn’s Blackmore Global and Richard Reinert’s Symphony Fund. So I would take issue with claims like “highly experienced” and “knowledgeable”.

If they were highly experienced and knowledgeable they would have known that, at the time I was being advised by Vilka in January 2015, Aktiva Wealth Management (later changed to Square Mile and now called Michalska Holding) was NOT regulated by the Czech National Bank. According to the CNB records, this didn’t happen until 5th May 2015 and then, only for insurance mediation and not for transferring pensions!

If Integrated Capabilities had been “highly experienced and knowledgeable” then they would have known the Symphony Fund – regulated in their own jurisdiction by their own regulator, the MFSA – was NOT permitted to be offered to me, a retail client. And they knew this because they had the Symphony documentation which clearly prohibited its promotion to UK retail clients.

I complained to the MFSA but they didn’t care and Malta’s “Ombudsman” equivalent – what they call the Office of the Arbiter for Financial Services – deters complaints because they have this small print that says if you lose, the other side can be awarded legal costs!

If Integrated Capabilities had been “highly experienced and knowledgeable” they would have known the Blackmore Global fund had never published audited accounts and still hasn’t to this day (December 2018). Something that in January 2015 caused Kreston (pension provider on the Isle of Man) to write to its members explaining their concerns over Blackmore Global and also stopped taking new members from Vilka.

So if they were “highly experienced and knowledgeable” then why did they allow all this to happen? It certainly had nothing to do with “motivation to do their utmost”. It is clear their only motivation was to take on as many members as possible – irrespective of which scammer introduced them and what unsuitable investments were made for them. Also, they claim to have a “long history and proven track record of providing expert and value for money multi-jurisdictional fiduciary solutions, so our clients and partners can have great peace of mind in the knowledge that our board of directors has over 100 years combined expertise in this field.” The proven track record is that they have taken on hundreds of new members per month from a known scammer – and the last thing their members have is peace of mind – far from it.