In the Pension Life office, we have been wondering how to get the information about pension scams more widely seen, heard and taken on board. We’d like to ensure the masses are educated and aware that pension scammers can strike from many angles, and with a variety of “deals”. Pension scammers must be stopped and together we can work towards this.

A quick Google search of the phrase “Pension Scam” shows no end of advice available, so why is this information not being spread to the public more widely and effectively?

Why was 2017 the WORST year for pension scams?

Google’s current top-ranking search return for the phrase “pension scam” is How to avoid a pension scam by Pension Wise. This site offers simple and basic information on how to spot a scam and how to report it.

This is followed by The Pensions Regulator (tPR) which, offers 5-step advice to protect a pension from pension scammers.

In third place, the Money Advice Service offers information on “How to spot a pension scam”. Money Advice highlight that scammers can be very good at disguising themselves as bona fide, regulated companies.

The FCA’s website comes in fourth, with their information on smart scams, advising people to be aware that the offer of a free pension review is often cause for concern and suspicion.

But, even with all this information out there, 2017 was still the worst year ever for pension scams. It seems that despite changes to regulations, scammers seem to come out on top nine times out of ten. Serial scammers are able to move onward and upward, scam after scam after scam. Officials, like the regulators, ombudsmen, arbiters and HMRC just stand idly by letting it happen again and again and again.

Maybe the problem is that the scammers are ever evolving in their behavior and tactics – and the authorities just can’t keep up. Pension Life came about because of the Ark pension liberation scam. But scamming tactics have moved on considerably.

We now we have noticeably less liberation and more investment scams where the introducer heads for the investment with the highest commissions, with no regard for the risk or fees that are applied to the fund.

Furthermore, if someone does approach you via a cold call claiming to be a viable company with a convincing sales pitch – how do you know if what they are saying is genuine? How do you know if they are a qualified financial adviser? Unfortunately, in the business of pensions and finance, the sad truth is that you need to: trust slowly; question quickly.

In the CWM case, victims saw unqualified, unregulated advisers placing low to medium risk investors’ entire funds into high-risk, fixed-term structured notes.

Fractional scamming is also on the up. Unqualified, unregulated firms posing as financial advisers act as “introducers” – and often introduce thousands of victims to outright scams. The funds then go through various other parties’ hands to ensure everyone gets their piece of the pie. Each party involved along the chain, creams their bit off the top of the pension fund, until the fund is a fraction of its former self. This means it will take years to get the pension back to its original state, let alone to start showing a profit.

Perhaps one of the most iniquitous aspects of pension and investment scams is the routine use of insurance bonds. (a significant part of the fractional scam and an unnecessary second “wrapper”). The life offices themselves are a big part of the pension scam industry.

Firms such as OMI, SEB, RL360 and Generali accept business repeatedly from unlicensed firms and known scammers. These so-called “life offices” (although they really ought to be called “death offices”) sit back and watch while these scammers gamble away the victims’ life savings on toxic structured notes and high-risk investments. Despite reporting on the inexorable destruction of the funds, firms like Generali et al just keep on taking their fees every quarter – and will sometimes do so until there is nothing left in the fund.

The best advice we can give, is to ensure you know exactly who you are dealing with and where your money will be going – every penny of it.

There is no such thing as “free”, and there will ALWAYS be commissions and fees on any pension transfer, legitimate or not. But however much it is – as in REALLY IS – the client needs to know and accept these costs. Many advisory firms conceal the real costs and the clients only find out what they are when it is too late, and the damage has been done.

Make sure you have everything in writing AND read it all – at least three times, if not more!

Make sure you understand everything: the costs, fixed terms, the risk level of investments – and if you don´t, then ask more questions.

Keep a regular eye on your fund; don´t trust any company 100%; make sure you know exactly what your fund is doing and do not ever be fobbed off with the explanation that any losses are “just paper losses”.

If in doubt – JUST SAY NO!!

I am writing a series of blogs about pensions, pension scammers and how to safeguard your pension fund from fraudsters. Please make sure you read as many as possible and ensure you know everything you should about your pension transfer. You only get one shot at getting it right – if you get it wrong, the damage may never be undone.

If we can ensure the masses are educated about pension scammers and financial fraud, we can help stop the scammers in their tracks – globally.

FT adviser published an article entitled, Cold calling ban approved by committee. However, do not get too excited as it hasn’t actually been approved by Parliament or got anywhere closer to being included in UK legislation.

Plans to ban cold calling were announced back in August 2017. Scammers love to cold call their victims and hard sell them their schemes. But it seems the number of people being targeted by scammers has risen immensely despite campaigns by the FCA and tPR.

In our opinion, there should be a blanket ban on cold calling and it should have happened many years ago. There really is no debate necessary. Scammers use cold calling techniques to lure their victims in. If they were not allowed to do this, there would be a significant reduction in scams.

Just this week, I have had two scam emails sent to me. One supposedly from HSBC (with whom I don’t bank!) and one supposedly from HMRC. The bank email told me I needed to log into my internet banking via their link and add my card details. The HMRC one promised me a tax rebate if I followed their link and input my credit card details!

To my relatively informed eye, it was obvious these were scam emails, but the offer of money back from HMRC did have a certain compelling lure to it. Several hundred pounds just before Christmas, yes please! However, I haven’t completed my tax return yet and very much doubt HMRC owe me anything. With tempting offers like this, it is easy to see how people can be lulled into a false sense of security, especially by a smooth talking salesman.

In so many scams, we hear the same thing; “I was called by a lovely man and he told me he could make my pension value increase if I transferred into…..but now my pension pot is worth less – much less.” The sad truth is that invariably the salesman is based offshore, is completely unqualified and only interested in the high commissions he will get from selling you a thoroughly inappropriate investment. He willprobably sell you a useless life bond too. Both of which will take a huge chunk of your pot before it has actually been invested anywhere.

The government has apologised for missing their deadline on passing this law, but I guess with all this Brexit chaos they are somewhat distracted. Given that they are unable to make a decision or deal on Brixit, I would guess they might struggle with passing a law that would protect their hardworking, tax-paying citizens.

I would also like to suggest that passing the ban might not be quite in the British government’s best interest. Often victims who have been scammed, have also liberated a cash amount out of their pension and this is taxable. 55% taxable to be precise. Therefore, by allowing the scams to go on, HMRC can coin in more tax revenues.

So, as we cannot count on our government to protect us from the cold calling scams, Pension Life is here to help.

Cold called? HANG UP!!!!

You don’t have to say anything, but if you do, make sure it’s something along the lines of:

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “scammers are criminals“. However, the sad truth is that most of them have not been prosecuted or jailed.

The vast majority of the well-known pension scammers are still roaming free, busy thinking up yet more life-destroying schemes to make them rich and the victims poor. Whilst the scammers enjoy champagne this New Year’s Eve, many victims will be worrying themselves sick about their bleak financial future.

The Pensions Regulator, the Serious Fraud Office, the Insolvency Service, crime enforcement agencies and courts all seem to drag their feet when it comes to actually bringing charges against these criminals. Yet we see people being locked up for renting out caravans to help vulnerable homeless families! I would love it if this was a short and sweet blog, with many happy endings. But, alas, the scams are plentiful and the victims are left uncompensated for their losses.

Let’s have a quick round up of where we are with the scams and scammers. And remember: all the thousands of victims want to see the scammers sent to jail and the keys thrown away so they can’t ruin any more innocent people’s lives.

5G Futures

5G Futures: in May 2013 Garry John Williams and Susan Lynn Huxley were suspended as trustees of the 5G Futures pension scheme, and from trust schemes in general. Pi Consulting was appointed as the new trustee by the Pensions Regulator.

About 400 people had invested a total of £20m into the 5G Futures scheme – which was invested in high-risk, illiquid off-shore investments, with insufficient diversification making them completely unsuitable for pension scheme investments. There was no due diligence exercised by Williams and Huxley – and the scheme records were a mess.

The scheme operated pension liberation through ‘loans’ to members. Williams and Huxley were found to have taken very high commissions on the investments – taking nearly £900,00 in one year alone.

One of the most worrying things, however, is that the pension scammers don’t just leave the pensions industry and dedicate themselves to helping their many distressed victims – they start up all over again:

Stephen Ward: (this will not be the last time you hear this name in this blog) was the mastermind behind this scam (dating back to 2010). It was his first known scam – but by no means his last one. What is left of the Ark fund, stands still frozen, in the hands of Dalriada Trustees, who continue to take their yearly costs and fees from what little is left. Dalriada has done nothing to ensure the scammers are prosecuted – saying it is “not within their remit”. The victims of the Ark scam also have the heavy hand of HMRC hanging over them. And let us not forget that it was HMRC who happily registered this scam and failed to withdraw the registration when they discovered that Stephen Ward was operating pension liberation fraud.

Dalriada has never reported Stephen Ward to the police as it is not “within their remit” to ensure the scammers are prosecuted.

In 2018 we saw Stephen Ward being banned from acting as a pension trustee. Eight years after his first scam, he has still not been imprisoned for the millions of pounds’ worth of life savings he has destroyed and the thousands of lives he has ruined.

Other prominent figures in the Ark scam were Julian Hanson – who went on to play a key role in the Friendly Pensions scam; George Frost who went on to operate a new pension liberation scam using truffle trees as investments; Andrew Isles who went on to sell his accountancy business, Isles and Storer to LB Group; Peter Moat of Blu Debt Management who went on to operate the Fast Pensions scam. None of these scammers has ever been convicted or jailed.

Axiom

Another pension liberation scam, which saw victims with HMRC tax demands of 55%. Rex Ashcroft of Wealth Protection International was one of the main introducers of this scam. According to his Linkedin profile, he offers business development strategy planning for the UK, Spain, Portugal and France. He also offers “day-to-day application of wealth protection strategies”. Ashcroft lied to Axiom victims telling them they could access part of their pensions and not pay tax on the cash they took out.

David Vilka, Phillip Nunn and Patrick McCreesh have never been convicted or jailed. Blackmore Global Group is still being promoted by Phillip Nunn! Nunn and McCreesh had been the main lead generators in the Capita Oak scam – earning nearly £1 million in the process.

This was another of Stephen Ward´s scams – on which he worked closely with his pensions lawyer Alan Fowler (ex Stevens and Bolton Solicitors) and his sidekick Bill Perkins. Ward carried out the transfer administration for this scam which was mainly operated by XXXX XXXX who offered victims 5% Thurlston “loans”. Over 300 victims are facing the partial or total loss of their pensions and are also now being pursued by HMRC for tax liabilities on the “loans”.

Capita Oak – like Ark – was placed in the hands of Dalriada Trustees. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward, Alan Fowler, Bill Perkins and XXXX XXXX have never been convicted or jailed (although XXXX XXXX is under investigation by the Serious Fraud Office).

Stephen Ward’s firm Premier Pension Solutions (in Moraira, Spain) was the “sister” firm of Continental Wealth Management, run by scammer Darren Kirby. This was one of the biggest single scams – known as CWM – with around 1,000 victims losing part or all of their life savings. Other scammers involved were Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway.

This scam was promoted by cold-calling victims and promising unrealistically high returns and “capital protection”. Darren Kirby and Anthony Downs used the victims’ funds to invest in totally unsuitable, high-risk, fixed-term structured notes. This scam saw huge commissions paid by the life offices – Old Mutual International, SEB, and Generali – as well as by the structured note providers: Leonteq, Commerzbank, Royal Bank of Canada, and BNP Paribas to this unregulated firm. Let us not forget that this was without question financial crime and was facilitated by the life offices.

Old Mutual International, run by ex IoM regulator Peter Kenny, was the leading life office which facilitated the CWM scam. Generali and SEB also routinely accepted business from these known scammers and unlicensed advisers.

Stephen Ward, Darren Kirby, Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway have never been convicted or jailed.

James Hay and Suffolk Life were accepting Elysian shares for liberation purposes

Another Stephen Ward creation which was operating 80% liberation with the full cooperation of the SIPPS providers James Hay and Suffolk Life. The SIPPS providers and the victims could face tax charges of up to £20 million from HMRC.

Despite clear evidence that Stephen Ward pushed this scam in emails to Alan Fowler and Bill Perkins, neither Ward nor Fowler nor Perkins have ever been prosecuted or jailed.

A New Zealand QROPS scam with Marazion pension loans

When Ark got shut down, Stephen Ward went straight to New Zealand to set up his next pension liberation scam with Simon Swallow of Charter Square. A further 300 victims were scammed out of over £10 million and conned into Marazion “loans” AND locked into the Evergreen scheme for five years. After the five years victims were told: ´Despite our best efforts, Evergreen has not been as successful as we had originally hoped.´ Evergreen was wound up April 208.

This scam was promoted by Darren Kirby’s Continental Wealth Management which cold called the victims.

Stephen Ward, Darren Kirby, and Simon Swallow have never been convicted or jailed.

It was determined that there is no doubt this was a scam.

Peter and Sara Moat and their accomplices have never been convicted or jailed.

Friendly Pensions Limited (FPL)

Back in January of 2018, the Pensions Regulator asked the High Court to act on their behalf in the Friendly Pensions matter. Scammers: David Austin, Susan Dalton, Alan Barratt and Julian Hanson (also involved in ARK) were ordered to pay back £13.7 million they took from their victims and banned from being pension trustees. However, Dalriada the independent trustee appointed by TPR to take over the running of the schemes, is in charge of confiscating the scammers’ assets for the benefit of their victims. (Who knows how long this could take: how long is a piece of string?) As yet, no compensation has been offered to the victims.

David Austin, Susan Dalton, Alan Barratt and Julian Hanson and their accomplices have never been convicted or jailed. However, there have recently been some arrests – so let us hope this results in maximum sentences.

Two bogus “occupational pension schemes” set up for pension liberation fraud by Stephen Ward after the Evergreen QROPS scam hit the rocks (when HMRC removed Evergreen from the QROPS list). Victims have no idea where or how their pensions are invested. The pensions are allegedly invested in “The Treasury Plus Fund” (whatever that might be – and it is not likely to be anything good) and the trustee is Ward’s bogus trustee firm Dorrixo Alliance.

Nobody knows the total aggregate value of lost pensions and tax liabilities Ward has caused – we hazard a guess at a figure in the region of £100 million +.

Another double act by Stephen Ward and XXXX XXXX. This was the “sister” scheme to Capita Oak. Ward did the transfer administration – from safe, well-known and regulated pension providers to this bogus occupational scheme run by XXXX.

Neither Stephen Ward nor XXXX XXXX has ever been convicted or jailed.

Another pension liberation scam – placed in the hands of Dalriada Trustees by the Pensions Regulator.

Incartus was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported the scammers to the police as it is not “within their remit” to ensure the scammers are prosecuted.

None of the Incartus or Bluefin trustees scammers has ever been convicted or jailed.

£11.9 million worth of transfers were made, with the victims receiving approximately 50% of their pension as a loan and the promise of the rest being invested into a high-interest generating SIPPS. The loans were made from the pensions and therefore the victims have the usual HMRC tax demand letters. Further to the victims’ misery, the other 50% of the funds was not invested as promised. Most of the funds were swallowed by high commissions paid to the scammers.

None of the KJK Investments/G Loans scammers has ever been convicted or jailed.

Another of Stephen Ward’s many pension scams, this one was courtesy of his bogus pension trustee firm Dorrixo Alliance, his accomplice Gary Barlow at Gerard Associates, and introducers at Viva Costa International. Like Ward´s other scams, London Quantum scam was never set up for the benefit of the victims, but in the interests of Stephen Ward and his team of scammers to earn the maximum amount of commission out of the toxic, illiquid, high-risk investments.

The London Quantum scam is now in the hands of Dalriada Trustees.

London Quantum – like Ark, Capita Oak and Fast Pensions – was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward and Gary Barlow have never been convicted or jailed.

This pension liberation scam dating back to 2013 and 2014, involved around £1m of victims pension funds. Anthony Locke, was sentenced to a five-year jail term and Ray King, 54, who was employed by Lock, was given a three-year jail sentence.

It is great that these two crooks received jail terms, however, they are relatively “small fry” in comparison to the other serial scammers who are still walking free! The question remains: why have two minor players such as Locke and King been convicted and jailed while the “big fish” remain free to keep on scamming?

116 victims were scammed out of their pensions by James Lau of FCA-regulated Wightman Fletcher McCabe. Victims were assured the loans they were given did not come from their pension funds and would not be taxable by HMRC. The trustees of the scheme – Peter Bradley and Andrew Meeson (both ex HMRC) of Tudor Capital Management – were jailed for eight years for cheating the Public Revenue. James Lau is currently under criminal investigation by the Insolvency Service. The victims are awaiting a verdict on whether they will still have to pay the tax penalties.

James Lau has not yet been convicted or jailed – although he is clearly a wanted man.

This scam was facilitated by STM Fidecs in Gibraltar – one of Europe’s biggest QROPS providers. The regulator did order Deloittes to carry out an inspection into STM Fidecs’ books, but no action was taken against STM Fidecs for their part in this scam.

STM Fidecs accepted transfers into the QROPS by UK-resident victims “advised” by XXXX XXXX – even though he was not licensed to give financial advice. And then XXXX’s clients were 100% invested in XXXX’s own fund.

XXXX XXXX has not yet been convicted or jailed – although he is clearly under investigation by the Serious Fraud Office.

Another of the schemes under investigation by the SFO. This liberation scam with more than £3 million worth of (now worthless) investments was registered and administered by Stephen Ward.

Windsor Pensions

A no-frills pension liberation scam run by Florida-based Steve Pimlott. This scam has been going on for years and there is no sign of any let up – despite the fact that the regulators and ombudsman are well aware of Pimlott’s modus operandi. Pimlott doesn’t bother with any attempt to conceal the loans with fancy “loans” or complex mechanisms to try to “distance” the liberation from the pension transfer. He uses QROPS and a fraudulently-set-up bank account in the Isle of Man (of course!). HMRC catches many of the victims and charges them 55% tax on the liberated amount. Pimlott charges around 15% for the liberation.

Steve Pimlott has not yet been convicted or jailed

What a sorry state of affairs that out of all the pension schemes I have mentioned here, only one of them has seen the scammers jailed. Serial scammers like Stephen Ward and XXXX XXXX seem to slip the noose of justice again and again.

Long-term savings plans by Friends Provident, Generali, Zurich, Hansard and RL360. These have been around for years and are typically mis-sold by seedy, unregulated advisory firms. Why don’t we come up with an alternative? THE LONG-TERM SAVINGS PIG!

Roughly speaking, the con artists at Friends Provident, Generali, Zurich, Hansard and RL360 structure these products so that for every two pounds saved, one pound goes to the life office and the spiv who sold the plan to the victim in the first place.

The adviser earns a packet by selling these useless plans and few victims continue saving for more than a few years – long before the end of the term. Pretty quickly, the con artists’ clients realise they’ve been scammed and that they’ve inadvertently signed up to an expensive, unworkable plan with no flexibility. They really would have been better off sticking their money under the mattress.

So here’s my suggested alternative: the LONG-TERM SAVINGS PIG:

You see, the problem with most long-term savings plans is that you are locked in and there is no flexibility. Plus there are heavy penalties and half of what you save goes in fees and commissions.

Imagine being able to save what you want, when you want, for free! All you have to do is be strict with yourself and save as much as you can, regularly and generously.

The problem is, of course, that so many offshore advisory firms sell products – rather than provide advice. Advisers earn huge commissions from mis-selling these appalling long-term savings plans – and ruin their clients in the process.

After as little as a year or two, the victims realise they’ve been conned and that they are simply pouring their hard-earned money into the pockets of the adviser and the life office.

In a perfect world, these dreadful products should be banned. All the advisers who have conned so many victims into believing they are paying into a flexible plan which is good value for money should be prohibited from ever working in financial services again. And the rogue life offices should be brought to justice and made to refund the victims’ money.

The reasons why these savings products don’t work are:

Few people can guarantee they will be able to save the contracted amount each month for the agreed period. People’s earnings do fluctuate and circumstances change.

Few people actually realise what they are signing up to. The advisers don’t tell them how expensive and inflexible the plans are.

Few people understand that half of what they save will be eaten up by fees and commissions.

Most people who get conned into these plans end up abandoning them and writing off what they have lost.

Remember, it’s your money and your life. Don’t get conned into giving half your savings to the scammer and the life office.

Just to make things crystal clear, if you sign up to a 25-year savings plan with one of the leading life offices, you will pay the following amount of fees over the life of the plan:

46.64% Friends Provident Premier 47.80% Generali Vision 48.07% Zurich Vista 51.28% Hansard Vantage 51.68% RL360 Quantum

So, if you save a total of £366,600 over 25 years with RL360, you will pay them (and your adviser) £189,460 in fees and commissions.

All pension and investment scams have one thing in common: if the pension scam victims had asked the offshore advisers some or all of these 10 essential questions, they might not have lost their life savings to the scammers.

Here at Pension Life, we are working hard to help educate the masses and stop pension scammers in their tracks worldwide. By arming and informing the public, and teaching them how to spot the scammers and avoid being scammed, we can help put a stop to these crimes.

With the scammers outsmarted, there will hopefully be fewer pension scam victims!

We have put together this cartoon which provides you, the investor, with 10 essential questions to ask your offshore adviser before you sign your precious pension fund over. Knowing what questions to ask could mean you do not become the next pension scam victim.

1. Pension Life has covered what qualifications your adviser needs to give pension advice. The adviser should also be able to show you their certificates and be registered with the governing body that awarded them – typically CII or CISI qualifications. We have created a series of blogs “firm name – qualified and registered?” which cover many offshore advisory firms and their team members. They show the firms that list employees who claim qualifications but are not registered and have failed to supplied proof and which firms are transparent. Some firms are happy to work with us and be 100% transparent and demonstrate that their team of advisers are fully qualified and registered.

2. Many offshore companies are regulated with an insurance licence ONLY and this is not sufficient to give pension and investment advice. They must have a licence to give advice on pensions and investments.

4. Insurance bonds are an expensive and unnecessary double wrapper on your pension. If it has already been invested in a SIPPS or a QROPS, insurance bonds are not needed. Insurance bonds are another way for the scammers to skim more commissions from your fund, putting a dent in your start and end value. Life offices such as Old Mutual International, Generali and RL360 are among the firms (known as life offices) to be avoided.

5. Structured note providers such as Leonteq, Nomura, Royal Bank of Canada and Commerzbank should be avoided. These companies are linked to previous pension scams and many victims have seen their pension funds destroyed with these high-risk, fixed-term notes, that are totally unsuitable for a pension fund. Often these structured notes have high commissions that make the ‘adviser’ big bucks.

6. Holding a DB pension puts you in good stead for your retirement. With a pension fund like this you are often better to ‘just do nothing’ and leave it as it is. Transferring it can lead to heavy charges and fees, meaning your fund becomes worth much less than before.

7. A pension is classed as a retail investment and needs to be invested in low to medium risk investments with a steady increase in value. Offers of high returns, especially in investments that use words like “renewable energies” or “property”, are illiquid and high risk. These types of investments are not safe for your pension. An example of this is the Elysian bio-fuels pension scam, facilitated by James Hay and Dolphin Trust – a German housing investment scheme – promoted to British steelworkers.

8. Time and time again, we see pension scam victims receiving the paperwork on the pension transfer ‘deal’ they have signed, only to realise that large fees and charges have been applied. The scammers are experts at hiding the charges and often quote the term: ‘free pension review’. Whilst they do not charge for all their visits and advice before you sign on the dotted line, they make up for this in transfer fees, commissions and often quarterly charges too! The quarterly charges will be applied no matter how your fund is doing. We have seen pension scam victims´ funds end up in negative equity due to being placed into an inappropriate fund which causes losses and second, continuing fees being applied. (Fees are normally based on the start value of the fund).

9. With the technology we have today, like smart phone apps, many firms are offering instant access to the progress of your pension fund through their own app. Options exist to add funds or change your investments and total transparency of investments and progress; a company that offers this service is Pension Bee. You should also get quarterly statements and annual reviews so you can track the progress of your fund.

10. We have seen pension scam victims repeatedly contacting their so-called advisers to try to get information on the demise of their fund, only to meet dead end after dead end. Again, ensure you are using a fully licensed firm that has an admin, compliance and support team. Ensure you are able to get a set of contact details (if not two!) and that there is a ‘real’ address and a landline – scammers often use PO boxes and mobile numbers.

Remember, it is your pension and your investment; you are entitled to ask as many questions as you like. These essential questions to ask offshore advisers should be simple for any trustworthy and transparent adviser to answer quickly and effortlessly. If your adviser is in any way cagey, vague or tries to avoid the question altogether, just walk away. An adviser who is unwilling to be totally transparent could well be a scammer.

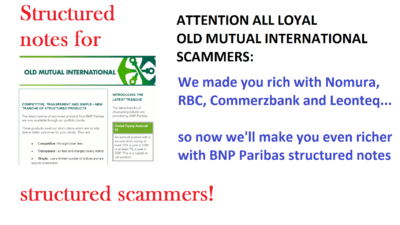

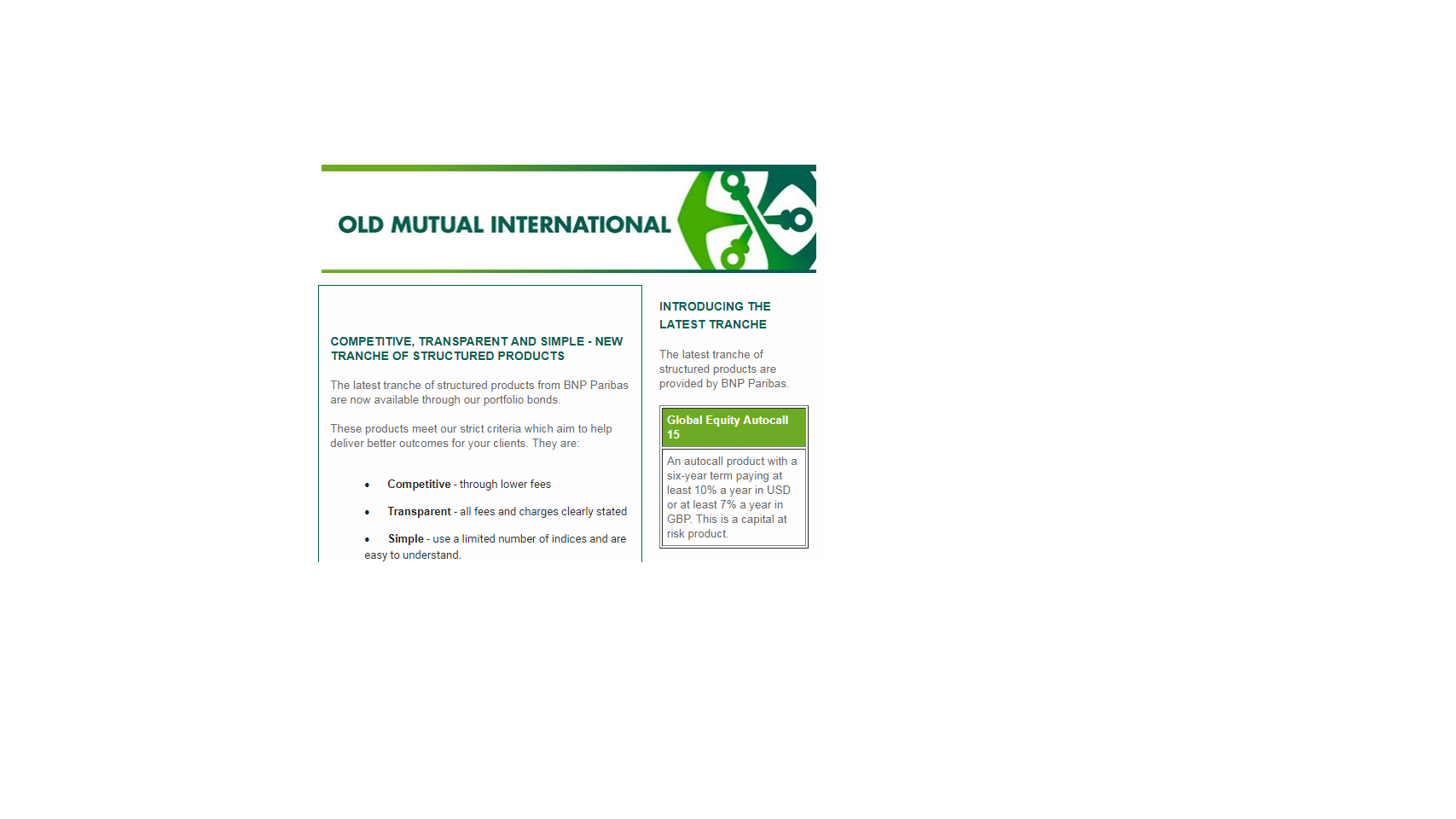

ROLL UP! ROLL UP! ME HEARTY SCAMMERS! OMI’S LATEST STRUCTURED NOTE SCAM IS ONLY AVAILABLE UNTIL SEPTEMBER 28TH SO GET A JIGGLE ON WHILE STOCKS OF THIS TOXIC CRAP LAST! WE ARE PROUD TO OFFER OUR VALUED SCAMMERS YET ANOTHER INVESTMENT SCAM

BY OLD MUTUAL INTERNATIONAL.

This wonderful investment scamming opportunity with OMI, is open to all scammers – you need no qualifications and don’t have to be regulated. If you want a bit of training in how to sell this rubbish inappropriate structured product to as many victims as possible, we can give you a quick five-minute whisper behind the bike shed. But, trust me, it is easypeasylemonsqueezy – just lie. Tell the victims about the “guaranteed 10% return” bit, but don’t tell them about the “capital at risk” bit.

So, what are you waiting for? You’ll earn 8% by selling your victims a useless OMI “PORTFOLIO” bond (don’t mention this is illegal in Spain) and then a further 8% from selling this toxic, high-risk BNP Paribas structured note (rubbish inappropriate structured product) which will tie your victims in for six years.

This will give you plenty of time to explain away the losses as “only secondary market values” or “only paper losses”. And by the time your victims realise what you’ve done to them, you’ll be long gone. And most of them will commit suicide anyway, so they won’t be coming after you any time soon.

BNP Paribas has a good reputation as being an ethical, solid company so that will certainly help you with sell these inappropriate structured products. Just remember, tell the victims as little as possible about this product and hide the commissions you will earn – they will never find out and by the time their life savings have all gone up in smoke you will be sunning yourself on a Caribbean island, far away from the misery of those whose retirement income you will have destroyed.

If the victims are ever organised enough to band together and form a group action, I’ll just promise to pay redress for their losses, organise a meeting and then cancel it at the last minute. That ought to buy you enough time to make your getaway.

Happy scamming – smiley face. Love from Pete

p.s. BTW, don’t worry about the email below the Mad Woman of Spain has sent out – most of the new victims will never have heard of her and by the time they do, it will be too late. You’ve only got until 28th September to scam as many suckers as possible, so don’t just stand there – SCAM AWAY ME HEARTIES!

p.p.s. Don’t worry about my quote about inappropriate structured products – I was just lying (something I’m pretty good at). With the announcement of new regulations in Malta for QROPS, International Adviser has quoted managing director of OMI (soon to be Quilter) Peter Kenny: “Old Mutual International is encouraging all market participants to help rid the industry of inappropriate structured products”

Paul, are you completely mad? OMI has been offering and buying inappropriate structured products for years and facilitating financial crime by scammers such as Continental Wealth Management. OMI bought £94 million worth of fraudulent notes by Leonteq – which paid the scammers an extra 2% in commission. So you must have been accepting business and investment instructions from other scammers besides CWM for at least six years between 2012 and 2016 – as well as for years prior to and subsequent to this period.

And now you are offering more structured notes so scammers can line their pockets and ruin more victims? Read your own marketing material Mate:

“An autocall product with a six-year term paying at least 10% a year in USD or at least 7% a year in GBP. This is a capital at risk product.”

You are a pathetic and revolting human being. Which bit of CAPITAL AT RISK don’t you understand?? OMI has already disgraced itself by offering, buying and selling these totally inappropriate structured products – scam products -, and caused millions of pounds’ worth of destruction to innocent victims’ life savings.

You, Peter Kenny, Steve Braudo and Paul Feeney are all as bad as each other – and none of you should be working in financial services. Your conduct is utterly sickening: you are now proposing to ruin more lives and you still haven’t paid compensation for the lives you have destroyed already.

How much commission are you paying the scammers on these toxic products? 6%? 8%? 10%?

Instead of behaving with decency and dignity and honouring Old Mutual International’s promise to pay redress for OMI’s past failures, you are now preparing to launch a whole new tranche of financial crime and inappropriate structured products.

You are all disgusting and this needs to be exposed and all of you outed for the evil scum you are.

Angie

From: Paul Evans – Old Mutual International <intmarketing@engage.omwealth.com> Subject: Competitive, transparent, simple – new tranche of structured products

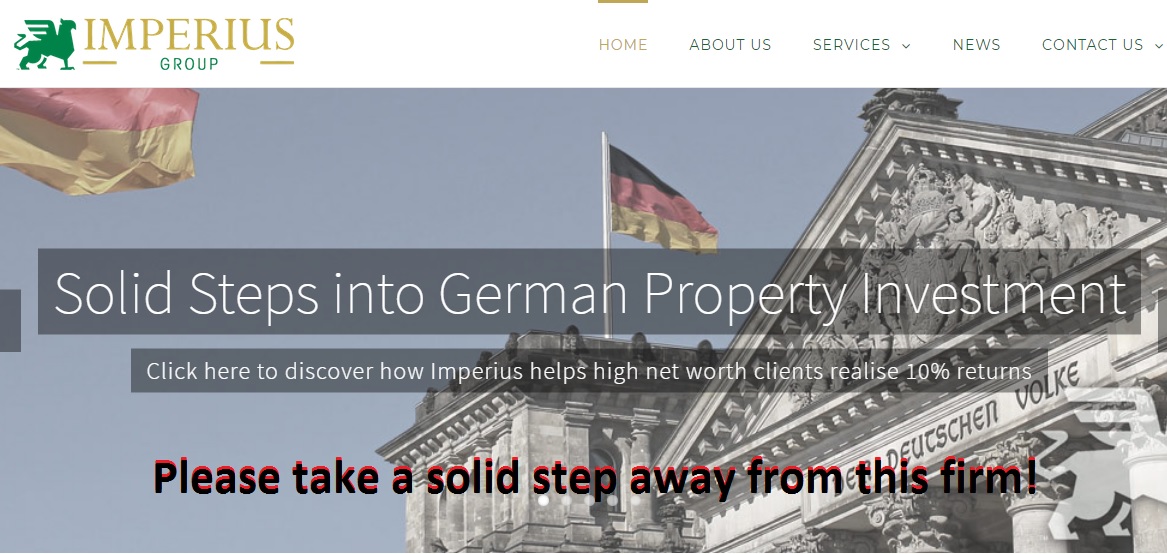

In my weekly hunt for the next firm to feature in my ´qualified and registered?´ blog series, I came across an advisory company that caught my attention: The Imperius Group, run by a fella named Tim Blogg, who claims to have retrained 25 years ago to offer pension and investment advice to expats.

The reason Tim Blogg´s company, The Imperius Group, flashed up on my red beacon radar was the fact that he listed his company in partnership with various life assurance offices including OMI (Old Mutual International) and Generali. Links to these companies, a well-read Pension Life blog follower will know, is not a good thing. They are also linked to RL360 and Hansard Global.

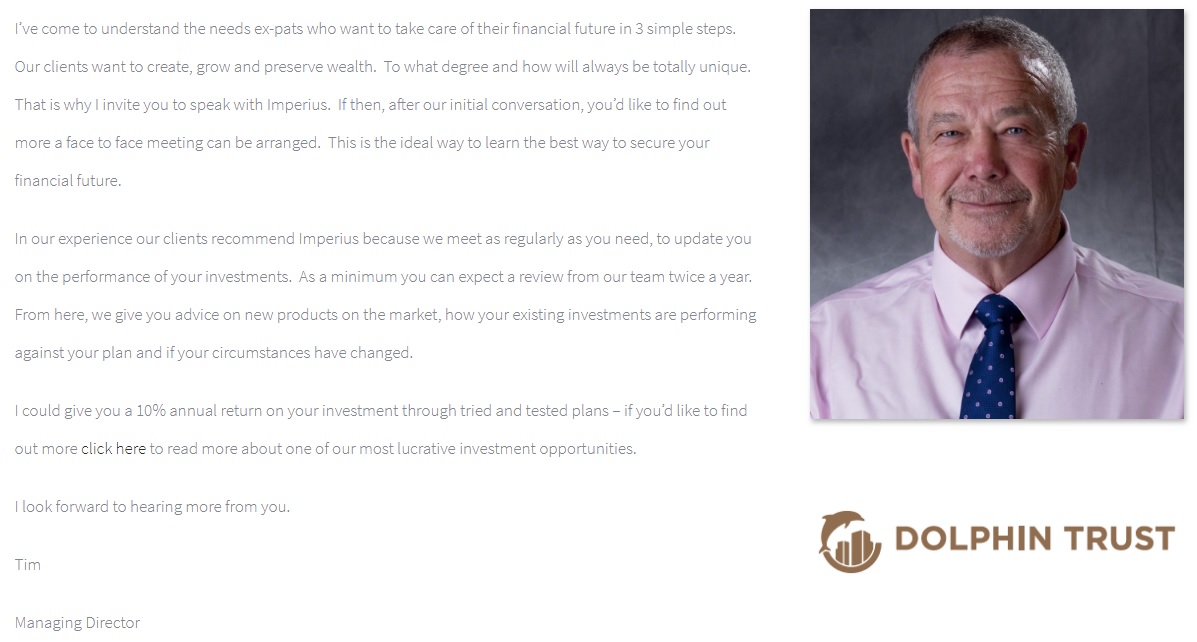

Tim Blogg also has a bright and shiny Dolphin Trust logo underneath the mug shot of him and a promise of:

“I could give you a 10% annual return on your investment through tried and tested plans – if you’d like to find out more click here to read more about one of our most lucrative investment opportunities.”

Tim Blogg offers “strong steps into German property investment”, through Dolphin Trust (loan notes).

Ring any bells?

British Steelworkers were duped into investing their DB pension schemes into – yes, you´ve got it – into an unregulated fund: Dolphin Trust (in Germany). Celtic Wealth Management acted as the introducers to this investment and Active Wealth – now collapsed – acted as the advisory company. This investment scam has left British Steelworkers trapped and at risk in this totally unsuitable, unregulated investment.

Dolphin Trust IS NOT regulated and there is no evidence to show The Imperius Group is either.

Tim Blogg, founder of The Imperius Group, DOES NOT APPEAR ON ANY REGISTER as a qualified and registered financial adviser.

Aside from Tim Blogg, the only other person who claims to work for The Imperius Group is a lady called Emma Allen, listing herself as, ´Employed as a Personal Assistant by iBOS working for the Managing Director of The Imperius Group Limited.´ The Imperius Group website quotes the term ´us´ regularly, but from what I have found, it would seem this company is pretty much a one-man unqualified band.

Once again, I am left wringing my hands in despair at the state of the offshore financial sector and at purported financial advisers like Tim Blogg.

However, at least I will sleep soundly tonight knowing that another financial advisory firm has been outed. The Imperius Group and Dolphin Trust are not the company to trust with your precious pension fund.

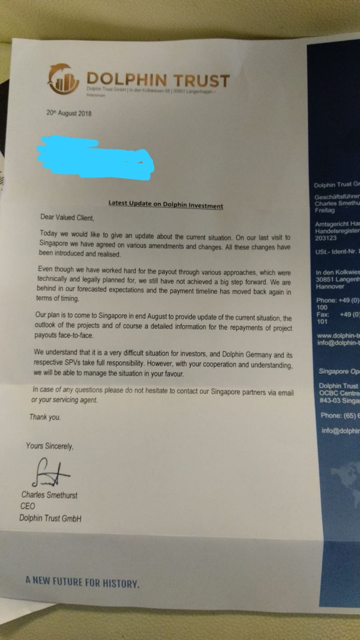

To demonstrate the serious concerns about investments in Dolphin Trust, this is a copy of a letter sent by Charles Smethurst CEO of Dolphin Trust to investors. It would seem that although some investments have reached their maturity, other investors are still waiting for their funds to be released. This raises questions about the liquidity of funds and also the possibility of Dolphin Trust going bankrupt. Maybe the victims will have a claim over the properties, if indeed the German properties they think they have invested in actually exist.

In many pension scams, we see the use of totally unsuitable, high-risk, for-professional-investor-only structured notes. These notes often offer the introducer high commissions. However, they are risky, fixed-term investments that often end in the loss of some – or even all – of the fund invested. Therefore, these types of investments are totally unsuitable for a pension fund. Firstly, let me explain what a structured note is, and then we can go through structured notes – knowing the risks.

So what the hell are structured notes? And why should retail investors say NO to them?

A structured note is an IOU from an investment bank that uses derivatives to create exposure to one or more investments. For example, you can have a structured note betting on the S&P 500 Price Index, the Emerging Market Price Index, or both. The combinations are almost limitless.

A pension fund is referred to as a retail investment, so it should be placed in a low to medium risk investment. Generally, structured notes are labeled high-risk, for professional investors only and, therefore, no pension fund should ever be invested into them.

Structured notes are frequently peddled by less-scrupulous financial advisers – as well as outright scammers – as a “high-yield, low-risk”, supposedly backdoor way to own stocks. However, regulators have warned that investors can get burned – which they frequently do. If the investment banks can flog it, they will make just about any toxic cocktail you can dream up. In reality, a structured note is an unsecured debt issued by a bank or brokerage firm – and the amount of money the investor might (or might not) get back is pegged to the performance of stocks or broad market indexes.

Say NO to structured notes for pensions!

With structured notes, there is no capital protection; no flexibility; no portfolio enhancement; no increased returns and no limit to the risk of loss of capital.

In the case of CWM, 1,000 people with 100 million pounds, were invested in structured notes and many of them lost large chunks of their funds. The CWM scam, headed by Darren Kirby, used structured notes with Commerzbank, Nomura, RBC and Leonteq, and many of the notes crashed.

John Rodgers fell victim to the CWM scam after being cold called by a salesman called Dean Stogsdill . His £202,000 pension pot was invested into high-risk, professional-investor-only structured notes referred to as “Blue Chip Notes”. Today John’s pension fund is worth just £60,000 (if he is lucky).

OMI help facilitate the unqualified, unlicensed and unregulated CWM scammers – victims of this scam were also tied into a useless, pointless insurance bond for ten years – courtesy of OMI. Whilst the value of these pension funds steadily plummeted, OMI stood idly by and watched it happen.

In the case of the Continental Wealth Management scam, the life offices – Old Mutual International, SEB and Generali, invested up to 1,000 victims’ life savings in structured notes. The majority of these toxic notes were from Commerzbank, Royal Bank of Canada, Nomura and Leonteq – some of which were, allegedly, fraudulent. Victims are facing huge losses – and a few have had their retirement savings wiped out entirely and a couple are now in negative territory due to the parasitic life offices continuing to take their quarterly fees (based on the original investment) as the investors are trapped into these spurious “bonds” for up to ten years.

We are now fighting to get the investors’ money back. But meanwhile, we must stress: do not use an advisory firm that uses structured notes. These toxic instruments are only for professional investors and should not EVER be used for ordinary, retail investors.

Investors’ trust is what gets violated in so many cases by irresponsible and negligent insurance companies such as Old Mutual International, SEB, Generali, RL360, Friends Provident International – and, of course, the firm in the Cayman Islands: Investors Trust. These companies – also known as “life offices” (although we prefer to call them “death offices” because they help destroy victims’ life savings – and sometimes cause the death of their distraught victims) – have a number of lethal practices which result in financial ruin for thousands of policyholders:

The life offices take business from any old known scammers – firms without proper licenses and with a known history of defrauding the public

The life offices will offer toxic, illiquid, risky funds – including UCIS funds – such as LM and Mansion on their platform (without doing any proper due diligence as to how quickly these funds can eradicate the life offices’ victims’ life savings)

The life offices will accept investment instructions from unqualified scammers who work for firms with no investment license – and, in some cases, with no insurance license either

The life offices will accept dealing instructions – often with fraudulently-copied or forged signatures – on dealing instructions for toxic assets such as professional-investor-only structured notes

A prime example of these vile practices was in the case of Mr. S – a driving instructor from Milton Keynes. His final salary pension scheme was transferred to a QROPS in Malta despite the fact that he was a UK resident and had no need for his pension to be transferred offshore. His “adviser” was David Vilka from a firm called Square Mile International Financial Services. This firm had an insurance license but no investment license. Therefore, Square Mile could legally sell insurance products such as dog insurance – but could certainly not provide investment advice.

Mr. S’ pension fund was then placed in a “life bond” with Investors Trust in the Cayman Islands. This was an entirely gratuitous transaction, as he had absolutely no need of such a bond – known to be a spurious life assurance policy used for what is called a “single premium” insurance contract. These bonds are illegal in Spain, since the Spanish Supreme Court has ruled that they are being used to hold investments in contravention of the nature of what insurance is supposed to be (i.e. risk for the insurer).

The entire fund – which represented Mr. S’ retirement savings – was then invested in two toxic UCIS funds (illegal to be promoted to UK-resident, retail investors) called Symphony and Blackmore Global. Investors Trust negligently accepted these investments from Square Mile – in the full knowledge that this was absolutely against the interests of the policyholder and that the “advisory” firm had no investment license.

After a protracted battle, waged with great tenacity and dogged determination, Mr S did indeed get back a large proportion of his fund. But he still suffered what can only be described as a harrowing experience which resulted in a total loss of a significant chunk of his pension to the scammers (who will have profited handsomely from scamming him in the first place).

Far from being contrite or apologetic, however, the scammer who risked Mr. S’ pension in the first place – David Vilka of Square Mile International Financial Services in the Czech Republic – showed no shame and made no attempt to recover the remainder of his victim’s pension. In fact, when I exposed Vilka’s vile scam, I was threatened by his two-bit American lawyer Douglas Davies of Lowell Davies LLP.

But what of the Cayman Islands-based life office – Investors Trust? Did they try to help Mr. S recover his serious losses? Did they offer him compensation for the significant distress he suffered at the hands of the scammers at Square Mile? Did they publish a statement demonstrating recognition of the damage done to victims’ life savings by investing in toxic crap like Blackmore Global on the instructions of scammers like David Vilka?

The answer, of course, is a resounding “no”. Investors Trust could have done so much to reform these illegal practices and expose the likes of scammer David Vilka who scammed not only Mr. S out of a big part of his pension, but also scammed hundreds of victims into the Hong Kong QROPS scam (many of which got invested in Blackmore Global).

Instead of showing any contrition or regret for facilitating financial crime, an idiot at Investors Trust called Lindsay Paris emailed me threatening to sue me for using a picture of David Vilka and John Ferguson posing as vulgar spivs at Las Vegas. This revolting photograph is, apparently, the property of Investors Trust:

“This is my second attempt to reach you regarding the copyright infringement on your website. Please have the image removed immediately or we will have no other choice but to seek legal action.

This is not the first time you have fraudulently misused private images and copyrights without authorization. You are imposing on our ownership rights and we would appreciate it if you would refrain from any future use of Investors Trust-owned materials. It is a serious violation which we will continue to pursue.

Lindsay Paris, Media and Communications Manager, Investors Trust Administration

lparis@investors-trust.com”

So, no apology for destroying victims’ life savings; no apology for taking business from a firm which was not regulated to give investment advice; no apology for investing a victim’s pension in a toxic UCIS fund run by known scammer Philip Nunn….just a complaint about a violation of their ownership rights of a picture of the scammers bearing the Investors Trust logo.

It is reported that Old Mutual International has put aside £69 million to pay compensation for their victims’ losses. May I suggest that Investors Trust should do the same thing – and then I will happily take down the vile picture of Vilka and Ferguson. But until then, it stays up. And if you want to sue me – go ahead: make my day.

Utmost Wealth and Generali PanEurope are set to merge with the help of Life Company Consolidation Group (LCCG). The plan is to re-brand as Utmost PanEurope. I wonder if this merger will do its utmost to ensure they manage and mitigate their future victims´ – sorry clients´ – risks, and protect their investments – as they certainly didn´t do so for their victims who suffered at the hands of CWM.

GPE chief executive Paul Gillett added: “We are proud of our performance over the last 20 years and have grown into one of the largest international companies in Ireland, with assets under management of over €10bn.

What a disgrace that Gillett can announce that he is “proud” of their performance over the last 20 years – proud of the misery and stress caused to the victims of the CWM pension scam? Proud of the fact that Generali have refused to take ANY responsibility for their victims´ losses.

Gillett goes on to say:

“The sale of the business to LCCG marks a very important step in our future development. Together, we represent one of the leading European providers of cross border wealth and corporate risk solutions with the potential to grow further across both current and new markets.”

With the responsibility of Generali being passed over to LCCG, here at Pension Life, we wonder if LCCG will be taking responsibility for Generali´s past victims as well. Will LCCG apply their corporate risk solutions to those who have already been put at risk? Generali on their own certainly didn´t apply a high standard of risk solutions when they placed CWM victims´ funds into high-risk, toxic, professional-investor-only structured notes.

Lets hope Utmost Wealth will do their utmost to sort out this utter disgrace caused by Generali´s negligence.

Humour me – you may consider me to be naive – but I believe that the ills of financial services (especially offshore) can be put right. All it takes is for the ethical stakeholders to outlaw the unethical ones. Yes, it will be a bit like something out of the Old Testament – but I firmly believe it can be done. And, more importantly, it MUST be done.

So many thousands of victims have lost part or all of their life savings already – and these people must be compensated. But, above all, future victims must be prevented.

Here’s my TOP TEN wishes that I want the Magic Financial Services Fairy to grant (as a matter of urgency):

Governments in the UK and all expat jurisdictions must wake up to scams – both offshore and at home. They must empower/galvanise law-enforcement agencies and give them the resources to tackle financial crime.

Regulators must put together effective regulations – and then ENFORCE them. Regulations on their own are worthless and pointless – the industry must be policed and failure to comply with regulations must be severely sanctioned.

Ceding pension providers must stop handing over thousands of pension transfers to scammers. The Scorpion campaign has had a negligible effect and all leading providers are still at it.

Advisory firms must be regulated – and not just for insurance. If all a firm does is sell insurance, that is fine. But if pension and investment advice is given, the firm must be properly regulated.

Advisers must be appropriately qualified. If they don’t have the right qualifications, they must demonstrate that they are studying and aiming to qualify within a reasonable, pre-determined time frame.

Investors with DB scheme transfers must get proper advice – avoiding flimflam which takes no responsibility for the end result of the transfer. QROPS providers must ensure they only accept business from regulated firms.

QROPS providers must also ensure they have understood and verified the members’ risk profiles – and then ensure that any investments made on behalf of those members are in line with their risk profile.

Life offices must stop accepting business from known scammers and unregulated firms – and cease investing victims’ life savings in unsuitable assets – such as structured notes and UCIS funds.

Life offices must pay redress to their victims for investment losses caused by negligence and fraud.

There must be a quality assurance system to which all offshore advisers, life offices, trustees and fund managers subscribe and adhere.

International Investment has written a jolly good article about the recent action taken by the UAE Insurance Authority – headed up by His Excellency Ibrahim Al Zaabi. I quote from Gary Robinson’s article:

“In a statement on the Arabic version on its website the IA has issued a circular confirming the suspension (of Holborn Assets) for a period of three months or until it is satisfied that the company has improved its performance.

According to Dubai-based sources that International Investment has been speaking to, the IA has written to regulated insurance companies notifying them of their action.”

I have no doubt that Holborn Assets will rise to the challenge magnificently and in a dignified manner – and will recognise the fact that it is time for the routine misuse of all insurance bonds in offshore financial services to come to an end. I also doubt Holborn Assets will sell any more RL360 products.

The Continental Wealth Management debacle must surely serve as a perfect example of how and why insurance bonds should not be used at all – and indeed how and why structured notes should be banned altogether. And yet, despite the Malta FSC’s lukewarm change in regulations to ban advisers without an investment license and limit structured notes to 30% of a portfolio, useless/pointless insurance bonds and toxic structured notes are very much the norm across the offshore financial services landscape.

The Eagle-eyed Sheikh Al Zaabi has obviously spotted something that regulators in all jurisdictions which affect British expats have turned a deliberate blind eye to. Insurance products can, have been, and are routinely abused. And the abusers often cause heavy losses to thousands of unfortunate victims. His Eminence also obviously recognises that turning a blind eye damages not only the jurisdiction in question, but also the reputation of financial services in general.

The FCAtakes no action even when their nose is rubbed into obvious fraud – and let the British Steel disaster happen under their very noses. In fact it took public-spirited independent financial services professionals such as Al Rush, Darren Cooke and Henry Tapper to take it on themselves to try to rescue the steelworkers while the scammers hovered like vultures. I would like to be proud to be British, but the FCA is a national disgrace and an embarrassment to all British citizens. I wouldn’t mind if the FCA was just lazy, but it simply doesn’t care about the interests of those who get conned and scammed.

The Guernsey FSC allowed many frauds, including trustees Concept Trustees to sell UCIS fund EEA Life Settlements even after the FSA “toxic” warning. And, of course, EEA Life Settlements itself. Then the stable door shut with a resounding clang as an ombudsman was brought in, but told not to hear any complaints prior to July 2013. This effectively excluded all the worst scams which were being carried out in Guernsey by the likes of Concept Trustees – which took business from Stephen Ward’s Premier Pension Solutions which neither had regulation nor professional indemnity insurance.

The Gibraltar FSC appears to actively encourage outright scammers such STM Fidecs – and when financial crime is brought to their attention they go fishing for a few small, wet fish. Talking of fish, I think it is very fishy that Paul Garner, now of the Gibraltar FSC, used to work for scammer XXXX XXXX at Global Partners Ltd – the firm that “advised” hundreds of UK-resident victims to transfer their pensions to an STM Fidecs QROPS. Then STM Fidecs allowed XXXX XXXX to invest 100% of 100% of these victims’ funds into his own UCIS fund: Trafalgar Multi Asset (now in liquidation). I genuinely don’t know at which point Paul Garner moved over from Global Partners Limited to the Gibraltar FSC……but I have a feeling his leaving do will be an exceptionally (and uncharacteristically) lavish affair – and I am very much hoping to be invited. I hear there will be something fishy on the menu and Garner’s good fortune will be toasted with something bubbly. I have no doubt the cleaners will effectively brush all the crumbs under the carpet after the party.

The Central Bank of Ireland will be put to the test when scammers SEB (formerly Irish Life) are put in the spotlight. CBI has known for years that SEB – led by Peder Nateus and Conor McCarthy – has been facilitating financial crime. SEB took £ millions’ worth of business from unlicensed scammers Continental Wealth Management and allowed the whole lot to be invested in toxic structured notes: “for professional investors only”. These notes – including the fraudulent Leonteq ones (over which OMI is now suing Leonteq) clearly warned of the “danger of loss of part or all of your capital”. And yet SEB sat there and watched while hundreds of CWM‘s clients’ victims’ life savings were destroyed – and did nothing. This has left many victims in despair and poverty – with some contemplating suicide.

Against this backdrop of extreme ineptitude and collusion amongst this collection of chocolate teapots, motorbike ashtrays and fishnet willy warmers, let us all hope that the UAE Insurance Authority shows all these no-hopers what effective regulation should look, smell and feel like.

Furthermore, if someone does approach you via a cold call claiming to be a viable company with a convincing sales pitch – how do you know if what they are saying is genuine? How do you know if they are a qualified financial adviser? Unfortunately, in the business of pensions and finance, the sad truth is that you need to: trust slowly; question quickly.

Furthermore, if someone does approach you via a cold call claiming to be a viable company with a convincing sales pitch – how do you know if what they are saying is genuine? How do you know if they are a qualified financial adviser? Unfortunately, in the business of pensions and finance, the sad truth is that you need to: trust slowly; question quickly. Make sure you have everything in writing AND read it all – at least three times, if not more!

Make sure you have everything in writing AND read it all – at least three times, if not more! FT adviser published an article entitled,

FT adviser published an article entitled,  To my relatively informed eye, it was obvious these were scam emails, but the offer of money back from

To my relatively informed eye, it was obvious these were scam emails, but the offer of money back from  So, as we cannot count on our government to protect us from the cold calling scams, Pension Life is here to help.

So, as we cannot count on our government to protect us from the cold calling scams, Pension Life is here to help.

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “ Neither Garry Williams nor Sue Huxley has ever been convicted or jailed.

Neither Garry Williams nor Sue Huxley has ever been convicted or jailed.

Fast Pensions

Fast Pensions

Another of Stephen Ward’s many pension scams, this one was courtesy of his bogus pension trustee firm

Another of Stephen Ward’s many pension scams, this one was courtesy of his bogus pension trustee firm  116 victims were scammed out of their pensions by James Lau of FCA-regulated Wightman Fletcher McCabe. Victims were assured the loans they were given did not come from their pension funds and would not be taxable by HMRC. The trustees of the scheme – Peter Bradley and Andrew Meeson (both ex HMRC) of Tudor Capital Management – were jailed for eight years for cheating the Public Revenue. James Lau is currently under criminal investigation by the Insolvency Service. The victims are awaiting a verdict on whether they will still have to pay the tax penalties.

116 victims were scammed out of their pensions by James Lau of FCA-regulated Wightman Fletcher McCabe. Victims were assured the loans they were given did not come from their pension funds and would not be taxable by HMRC. The trustees of the scheme – Peter Bradley and Andrew Meeson (both ex HMRC) of Tudor Capital Management – were jailed for eight years for cheating the Public Revenue. James Lau is currently under criminal investigation by the Insolvency Service. The victims are awaiting a verdict on whether they will still have to pay the tax penalties.

Long-term savings plans by Friends Provident,

Long-term savings plans by Friends Provident,  So here’s my suggested alternative: the LONG-TERM SAVINGS PIG:

So here’s my suggested alternative: the LONG-TERM SAVINGS PIG:

Remember, it’s your money and your life. Don’t get conned into giving half your savings to the scammer and the life office.

Remember, it’s your money and your life. Don’t get conned into giving half your savings to the scammer and the life office.

4. Insurance bonds are an expensive and unnecessary

4. Insurance bonds are an expensive and unnecessary  8. Time and time again, we see pension scam victims receiving the paperwork on the pension transfer ‘deal’ they have signed, only to realise that large fees and charges have been applied. The scammers are experts at hiding the charges and often quote the term: ‘free pension review’. Whilst they do not charge for all their visits and advice before you sign on the dotted line, they make up for this in transfer fees, commissions and often quarterly charges too! The quarterly charges will be applied no matter how your fund is doing. We have seen pension scam victims´ funds end up in negative equity due to being placed into an inappropriate fund which causes losses and second, continuing fees being applied. (Fees are normally based on the start value of the fund).

8. Time and time again, we see pension scam victims receiving the paperwork on the pension transfer ‘deal’ they have signed, only to realise that large fees and charges have been applied. The scammers are experts at hiding the charges and often quote the term: ‘free pension review’. Whilst they do not charge for all their visits and advice before you sign on the dotted line, they make up for this in transfer fees, commissions and often quarterly charges too! The quarterly charges will be applied no matter how your fund is doing. We have seen pension scam victims´ funds end up in negative equity due to being placed into an inappropriate fund which causes losses and second, continuing fees being applied. (Fees are normally based on the start value of the fund). ROLL UP! ROLL UP! ME HEARTY SCAMMERS! OMI’S LATEST

ROLL UP! ROLL UP! ME HEARTY SCAMMERS! OMI’S LATEST  So, what are you waiting for? You’ll earn 8% by selling your victims a useless OMI “PORTFOLIO” bond (don’t mention this is illegal in Spain) and then a further 8% from selling this toxic, high-risk BNP Paribas structured note (rubbish inappropriate structured product) which will tie your victims in for

So, what are you waiting for? You’ll earn 8% by selling your victims a useless OMI “PORTFOLIO” bond (don’t mention this is illegal in Spain) and then a further 8% from selling this toxic, high-risk BNP Paribas structured note (rubbish inappropriate structured product) which will tie your victims in for

Investors’ trust is what gets violated in so many cases by irresponsible and negligent insurance companies such as Old Mutual International, SEB, Generali, RL360, Friends Provident International – and, of course, the firm in the Cayman Islands: Investors Trust. These companies – also known as “life offices” (although we prefer to call them “death offices” because they help destroy victims’ life savings – and sometimes cause the death of their distraught victims) – have a number of lethal practices which result in financial ruin for thousands of policyholders:

Investors’ trust is what gets violated in so many cases by irresponsible and negligent insurance companies such as Old Mutual International, SEB, Generali, RL360, Friends Provident International – and, of course, the firm in the Cayman Islands: Investors Trust. These companies – also known as “life offices” (although we prefer to call them “death offices” because they help destroy victims’ life savings – and sometimes cause the death of their distraught victims) – have a number of lethal practices which result in financial ruin for thousands of policyholders: A prime example of these vile practices was in the case of Mr. S – a driving instructor from Milton Keynes. His final salary pension scheme was transferred to a QROPS in Malta despite the fact that he was a UK resident and had no need for his pension to be transferred offshore. His “adviser” was David Vilka from a firm called Square Mile International Financial Services. This firm had an insurance license but no investment license. Therefore, Square Mile could legally sell insurance products such as dog insurance – but could certainly not provide investment advice.

A prime example of these vile practices was in the case of Mr. S – a driving instructor from Milton Keynes. His final salary pension scheme was transferred to a QROPS in Malta despite the fact that he was a UK resident and had no need for his pension to be transferred offshore. His “adviser” was David Vilka from a firm called Square Mile International Financial Services. This firm had an insurance license but no investment license. Therefore, Square Mile could legally sell insurance products such as dog insurance – but could certainly not provide investment advice.

Far from being contrite or apologetic, however, the scammer who risked Mr. S’ pension in the first place – David Vilka of Square Mile International Financial Services in the Czech Republic – showed no shame and made no attempt to recover the remainder of his victim’s pension. In fact, when I exposed Vilka’s vile scam, I was threatened by his two-bit American lawyer

Far from being contrite or apologetic, however, the scammer who risked Mr. S’ pension in the first place – David Vilka of Square Mile International Financial Services in the Czech Republic – showed no shame and made no attempt to recover the remainder of his victim’s pension. In fact, when I exposed Vilka’s vile scam, I was threatened by his two-bit American lawyer

What a disgrace that Gillett can announce that he is “proud” of their performance over the last 20 years – proud of the misery and stress caused to the victims of the

What a disgrace that Gillett can announce that he is “proud” of their performance over the last 20 years – proud of the misery and stress caused to the victims of the  With the responsibility of Generali being passed over to LCCG, here at Pension Life, we wonder if LCCG will be taking responsibility for Generali´s past victims as well. Will LCCG apply their corporate risk solutions to those who have already been put at risk? Generali on their own certainly didn´t apply a high standard of risk solutions when they placed CWM victims´ funds into high-risk, toxic, professional-investor-only structured notes.

With the responsibility of Generali being passed over to LCCG, here at Pension Life, we wonder if LCCG will be taking responsibility for Generali´s past victims as well. Will LCCG apply their corporate risk solutions to those who have already been put at risk? Generali on their own certainly didn´t apply a high standard of risk solutions when they placed CWM victims´ funds into high-risk, toxic, professional-investor-only structured notes.

Governments in the UK and all expat jurisdictions must wake up to scams – both offshore and at home. They must empower/galvanise law-enforcement agencies and give them the resources to tackle financial crime.

Governments in the UK and all expat jurisdictions must wake up to scams – both offshore and at home. They must empower/galvanise law-enforcement agencies and give them the resources to tackle financial crime. Regulators must put together effective regulations – and then ENFORCE them. Regulations on their own are worthless and pointless – the industry must be policed and failure to comply with regulations must be severely sanctioned.

Regulators must put together effective regulations – and then ENFORCE them. Regulations on their own are worthless and pointless – the industry must be policed and failure to comply with regulations must be severely sanctioned.

.

. Advisers must be appropriately qualified. If they don’t have the right qualifications, they must demonstrate that they are studying and aiming to qualify within a reasonable, pre-determined time frame.

Advisers must be appropriately qualified. If they don’t have the right qualifications, they must demonstrate that they are studying and aiming to qualify within a reasonable, pre-determined time frame.

QROPS providers must also ensure they have understood and verified the members’ risk profiles – and then ensure that any investments made on behalf of those members are in line with their risk profile.

QROPS providers must also ensure they have understood and verified the members’ risk profiles – and then ensure that any investments made on behalf of those members are in line with their risk profile. Life offices must stop accepting business from known scammers and unregulated firms – and cease investing victims’ life savings in unsuitable assets – such as structured notes and UCIS funds.

Life offices must stop accepting business from known scammers and unregulated firms – and cease investing victims’ life savings in unsuitable assets – such as structured notes and UCIS funds.

International Investment has written a jolly good article about the recent action taken by the UAE Insurance Authority – headed up by His Excellency Ibrahim Al Zaabi. I quote from

International Investment has written a jolly good article about the recent action taken by the UAE Insurance Authority – headed up by His Excellency Ibrahim Al Zaabi. I quote from  The Gibraltar FSC

The Gibraltar FSC